According to a report from Goldman Sachs Research, advances in electric vehicle (EV) battery technology and falling prices for key metals are expected to drive down battery costs faster than previously anticipated. This accelerated decrease could make EVs significantly more affordable in the coming years, with cost parity with gasoline-fueled cars predicted to occur by 2026.

Global Battery Prices on a Downward Trajectory

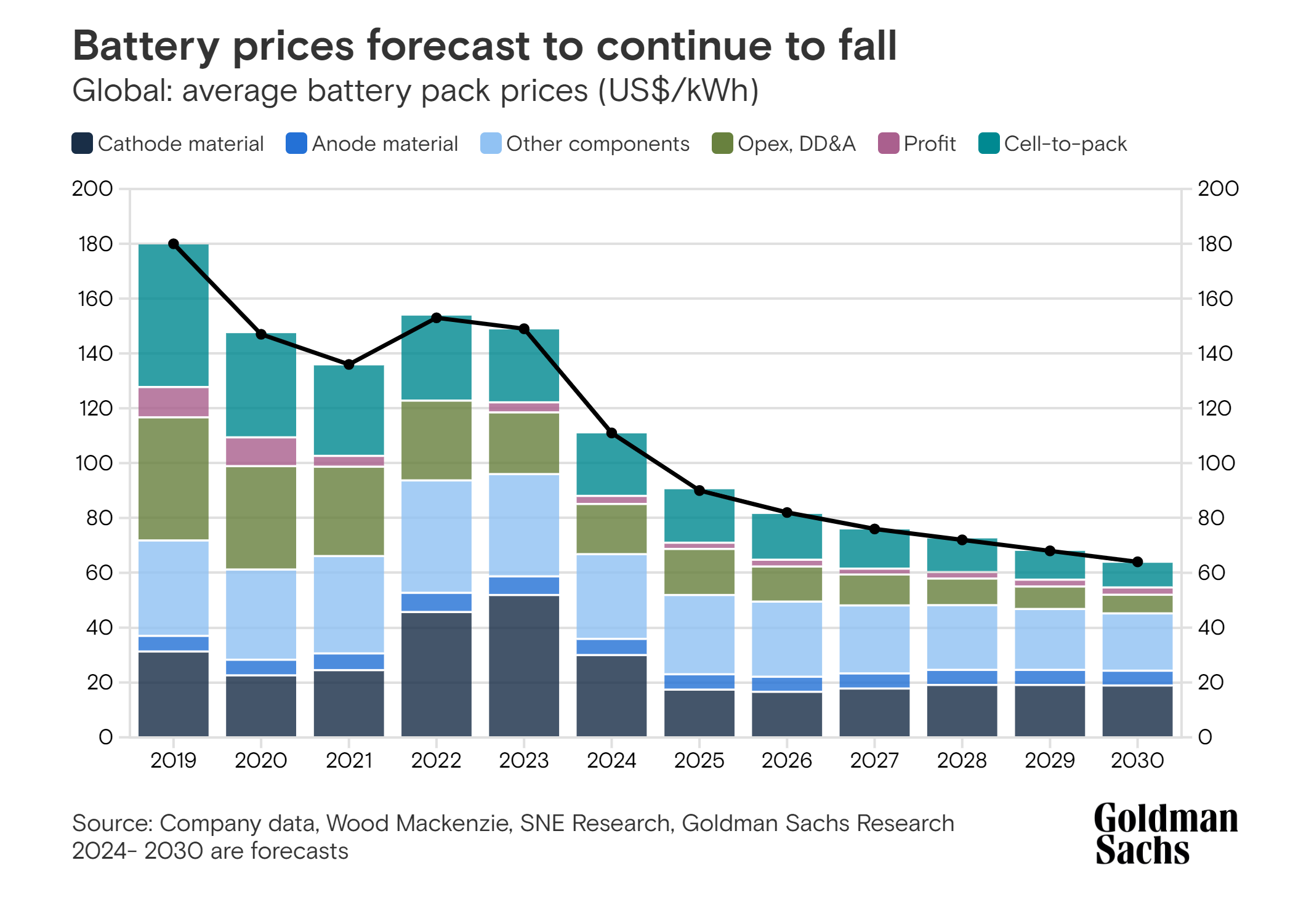

The global average battery price dropped from $153 per kilowatt-hour (kWh) in 2022 to $149 in 2023, and Goldman Sachs Research projects it will decrease to $111 by the end of this year. By 2026, battery prices could fall to around $80/kWh—a nearly 50% reduction from 2023 levels. This price point would allow battery electric vehicles (BEVs) to achieve total cost of ownership parity with gasoline-powered cars in the U.S., without the need for government subsidies.

Key Drivers Behind the Price Decline

According to Nikhil Bhandari, co-head of Goldman Sachs Research’s Asia-Pacific Natural Resources and Clean Energy division, two major factors are contributing to the faster-than-expected drop in battery prices. The first is technological innovation. New battery products being launched are offering around 30% higher energy density and come with lower production costs.

The second driver is the continued decline in the prices of battery metals, including lithium and cobalt. Bhandari noted that metals account for nearly 60% of a battery’s cost, and over 40% of the price decline through 2030 can be attributed to lower commodity prices. From 2020 to 2023, the industry experienced what Bhandari called “green inflation,” but this has since subsided, helping to drive down costs.

Technological Innovations Increasing Energy Density

Battery manufacturers have made significant strides in increasing energy density, largely through structural innovations. One such innovation is the shift toward “cell-to-pack” technology, which eliminates the need for traditional modules by packing larger cells directly into battery packs. This approach maximizes space efficiency, allowing for higher energy storage and reduced costs.

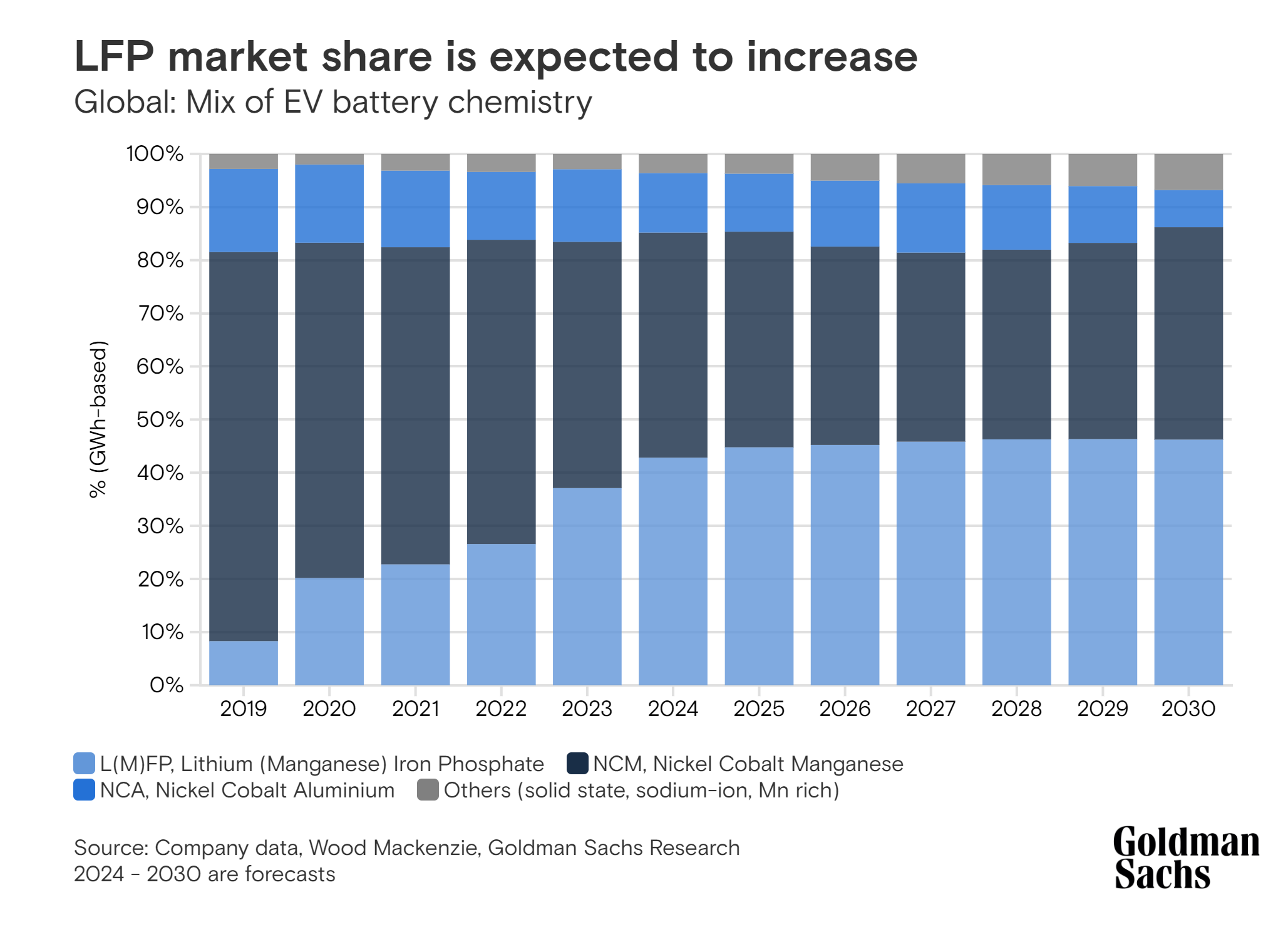

Currently, the market is dominated by lithium-based batteries. Nickel-based chemistries account for about 60% of the market, while lithium iron phosphate (LFP) batteries hold 35-40%. Sodium-ion batteries, the only non-lithium technology, currently occupy a small portion of the market and have not yet scaled up for mass production.

The Future of Solid-State Batteries

While solid-state batteries have been touted as a potential game-changer due to their ability to offer higher energy density and improved safety, their commercialization has been delayed. Initially expected to capture 5-10% of the market, solid-state batteries have faced challenges in transitioning from lab-scale production to mass manufacturing. As a result, their market debut has been pushed to the latter half of this decade.

In the meantime, existing lithium-based chemistries, particularly LFP batteries, are expected to continue gaining market share. Goldman Sachs has raised its forecast for LFP batteries, predicting they will capture 45% of the market by 2025, while nickel-based batteries will remain dominant in the high-energy density segment.

Challenges for New Entrants in the Battery Industry

The battery manufacturing industry presents significantbarriers to entry, making it difficult for new players to compete. It typically takes about 10 years to transition from research and development to the first production, with even more time required to achieve efficient mass production and high-quality yields. Even established companies that have been in the industry for 10 to 15 years are still struggling to break even.

Moreover, the market is currently controlled by five major companies, which account for nearly 80% of global battery production. These companies have been investing heavily in research and development, creating a cycle of intensified competition that makes it challenging for newer entrants to survive, particularly as they face a cyclical downturn in battery prices.

Will Lower Battery Prices Boost EV Demand?

The decline in battery prices is expected to significantly impact EV demand, especially once price parity with internal combustion engine (ICE) cars is achieved. In the past, the cost premium for EVs was offset by long-term fuel savings, but falling EV prices are now prompting consumers to factor in resale value concerns. Many buyers anticipate that EV prices will continue to drop, leading to faster depreciation for used electric cars.

Goldman Sachs’ recent analysis accounts for these concerns, but the firm still expects cost parity to be achieved by 2026, assuming a high oil price environment. Although near-term EV demand may rely heavily on regulatory measures, particularly in 2024, demand is projected to surge in 2026, driven by consumer economics rather than government mandates. This year could mark the beginning of widespread EV adoption.

Conclusion

The rapid decline in EV battery prices and ongoing technological advancements signal a pivotal moment for the electric vehicle industry. By 2026, EVs are expected to achieve cost parity with gasoline-powered cars without relying on subsidies, potentially ushering in a new era of mass EV adoption. For battery manufacturers and automakers alike, the coming years will be crucial for innovation and market expansion.