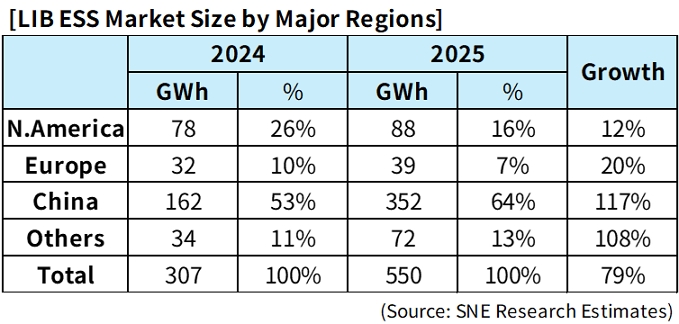

Explosive Growth in the Global Storage Market

According to data released on January 28 by SNE Research, a prominent market research firm, global shipments of Lithium-Ion Batteries (LIB) for Energy Storage Systems (ESS) reached 550 GWh in 2025. This figure represents a remarkable 79% year-on-year growth compared to the 307 GWh recorded in 2024, highlighting the accelerating global demand for energy transition technologies. Unlike EV batteries which are consumer components, ESS batteries are deployed in regional infrastructure projects, meaning shipment volumes directly reflect actual installation capacity and market activity.

China Dominates the Regional Landscape

Regionally, China solidified its position as the global leader in 2025, with its domestic ESS market reaching a massive 352 GWh, accounting for 64% of the global total. Driven by robust government policies supporting renewable energy integration, the Chinese market achieved a staggering year-on-year growth rate of 117%, outpacing all other regions. In contrast, while North America remained the second-largest market with 88 GWh (16% share), it recorded the slowest growth among major regions at just 12%, signaling a significant slowdown.

North American Market Slows Amid Policy Barriers

The sluggish growth in the North American market is largely attributed to supply chain disruptions caused by the U.S. government’s high-tariff policies against China. Trade restrictions targeting cost-effective Chinese Lithium Iron Phosphate (LFP) batteries have increased project costs and delayed deployment timelines in the region. Meanwhile, the European market maintained steady progress, with shipments reaching 39 GWh in 2025, reflecting a 20% growth rate and capturing a 7% global market share.

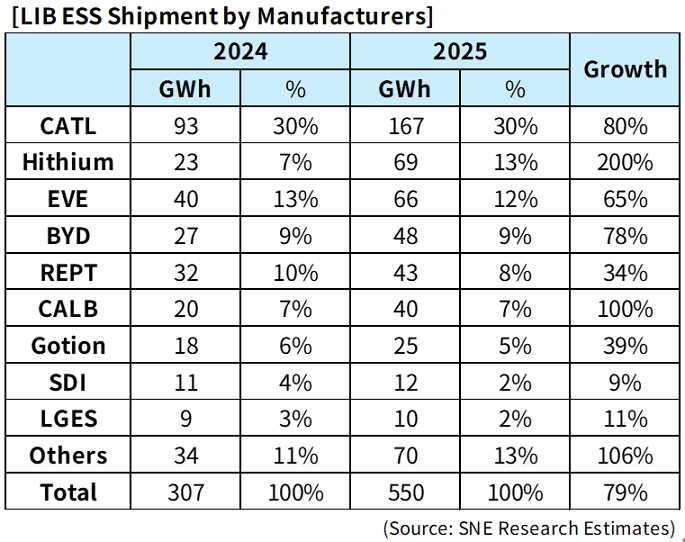

Chinese Manufacturers Sweep the Top Seven

In the competitive landscape of manufacturers, Chinese battery companies demonstrated overwhelming dominance, sweeping the top seven positions in global shipment rankings. These seven companies combined to capture a massive 83.3% of the global market share, effectively controlling the supply chain for energy storage batteries worldwide. CATL maintained its undisputed leadership, shipping 167 GWh to secure a 30% market share, with an impressive 80% increase in shipments compared to the previous year.

Hithium Emerges as the Breakout Star

Amidst fierce competition, Hithium delivered the most standout performance, surging to rank second globally with shipments of 69 GWh and a 13% market share. The company recorded an extraordinary 200% year-on-year growth rate, the highest among the top ten manufacturers, showcasing its explosive potential in the dedicated energy storage sector. EVE Energy and BYD followed in third and fourth places, shipping 66 GWh and 48 GWh respectively, both maintaining solid growth trajectories.

Korean Battery Makers See Market Share Erode

In sharp contrast to the expansion of Chinese firms, South Korean battery manufacturers saw their presence in the global ESS market shrink further, falling to 8th and 9th place. Samsung SDI and LG Energy Solution (LGES) combined for just 22 GWh of shipments in 2025, with their aggregate market share dropping to approximately 4%. Although their shipment volumes saw slight increases (9% and 11% respectively), they lagged far behind the market average, leading to a diminished influence on the global stage.

Technology Choice Defines the Market Divide

The divergence in performance stems primarily from technology choices: Chinese firms have championed LFP batteries, which are preferred for ESS due to their superior safety profile and cost-competitiveness. Conversely, Korean manufacturers have long focused on ternary batteries (NCM/NCA), which offer high energy density but struggle to compete on cost and safety in the stationary storage sector. Furthermore, the contraction of the domestic South Korean ESS market, traditionally a stronghold for local firms, has deprived them of a critical revenue base.

Strategic Pivots and Future Outlook

Facing the comprehensive dominance of LFP technology in energy storage, Korean battery giants are initiating strategic pivots, targeting the North American market for recovery. Plans are underway to convert existing EV battery production lines in the U.S. to LFP lines, aiming to bypass tariff barriers and meet local demand for affordable storage solutions. However, analysts suggest that outside of North America, Chinese LFP batteries will likely remain the mainstream choice globally, leaving Korean firms with a steep hill to climb.