Global Market: Breaking the 1,187 GWh Threshold

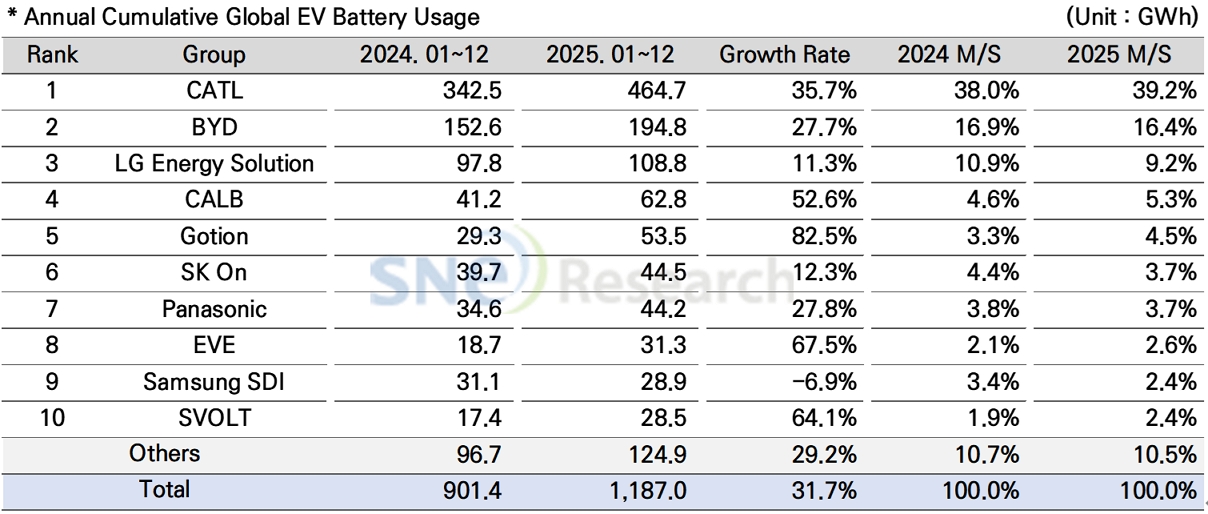

From January to December 2025, the total amount of energy held by batteries for registered electric vehicles (EV, PHEV, HEV) worldwide was approximately 1,187 GWh. This represents a robust 31.7% year-on-year (YoY) growth, signaling that despite regional demand fluctuations, the global electrification trend remains resilient.

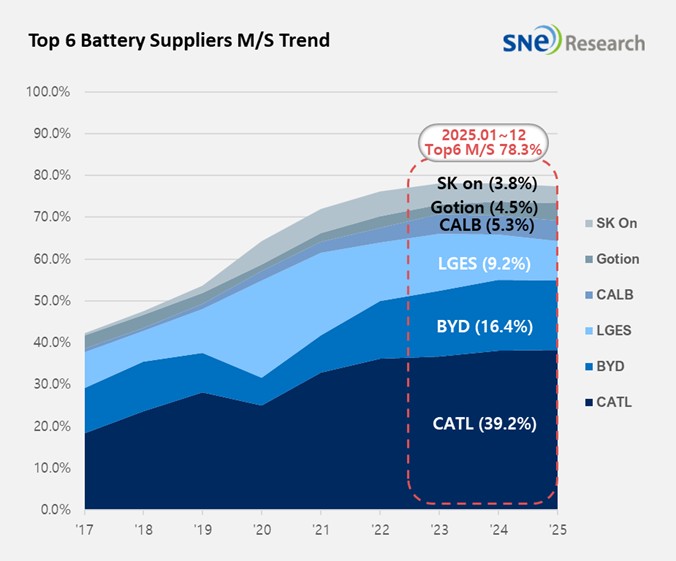

The market continues to centralize, with the Top 6 suppliers accounting for 78.3% of the total market share. This concentration suggests that large-scale manufacturers are successfully leveraging cost competitiveness and supply chain vertical integration.

Chinese Leaders: The Absolute Dominance of CATL and BYD

CATL firmly maintained its position as the global leader, recording a battery usage of 464.7 GWh, a 35.7% increase compared to the previous year. Its market share rose to 39.2%, supported by a massive client base including Tesla, BMW, Mercedes-Benz, and several major Chinese OEMs.

BYD ranked second globally with 194.8 GWh of usage, growing 27.7% YoY. Notably, BYD’s battery usage in Europe soared by 201.4% in 2025, reaching 14.9 GWh as it rapidly expands its presence in international markets.

South Korean “K-trio”: Market Share Hits New Lows

The combined market share of LG Energy Solution (LGES), SK On, and Samsung SDI dropped to 15.4%, a 3.3 percentage point decline YoY. LGES remained 3rd globally with 108.8 GWh (11.3% growth), but its growth was constrained by sluggish sales of certain Tesla models.

SK On ranked 6th with 44.5 GWh, showing a 12.3% growth supported by Hyundai and Volkswagen. However, the plummeted sales of the Ford F-150 Lightning and the slowdown in U.S. demand are expected to be burdening factors for its future volume.

Samsung SDI recorded a 6.9% decrease in usage, falling to 28.9 GWh and ranking 9th. While sales of the BMW i4 and i5 were strong, the overall decline was driven by sluggish sales of the Audi Q8 e-Tron and Rivian vehicles.

Emerging Black Horses: CALB and Gotion Post High Growth

CALB and Gotion have emerged as major contenders, ranking 4th and 5th respectively. Gotion posted the highest growth among the top players at 82.5%, while CALB grew by 52.6%, further solidifying Chinese dominance in the mid-market segment.

Other Chinese firms like EVE, SVOLT, and Sunwoda also showed significant growth rates exceeding 60%. This trend indicates that Chinese manufacturers are successfully diversifying their product portfolios beyond their domestic market.

Next-Gen Technology: The Race for Sodium-ion and ESS

To maintain its edge, CATL is accelerating the commercialization of sodium-ion batteries, with full-scale mass production planned for 2026. These batteries are expected to be applied in both passenger and commercial vehicles due to their cost competitiveness and superior low-temperature performance.

Meanwhile, companies like Panasonic and LGES are strategically pivoting toward Energy Storage Systems (ESS). This shift aims to buffer risks associated with the EV demand slowdown and tap into the increasing power demand from AI data centers and grid stabilization.