A Record-Breaking Streak

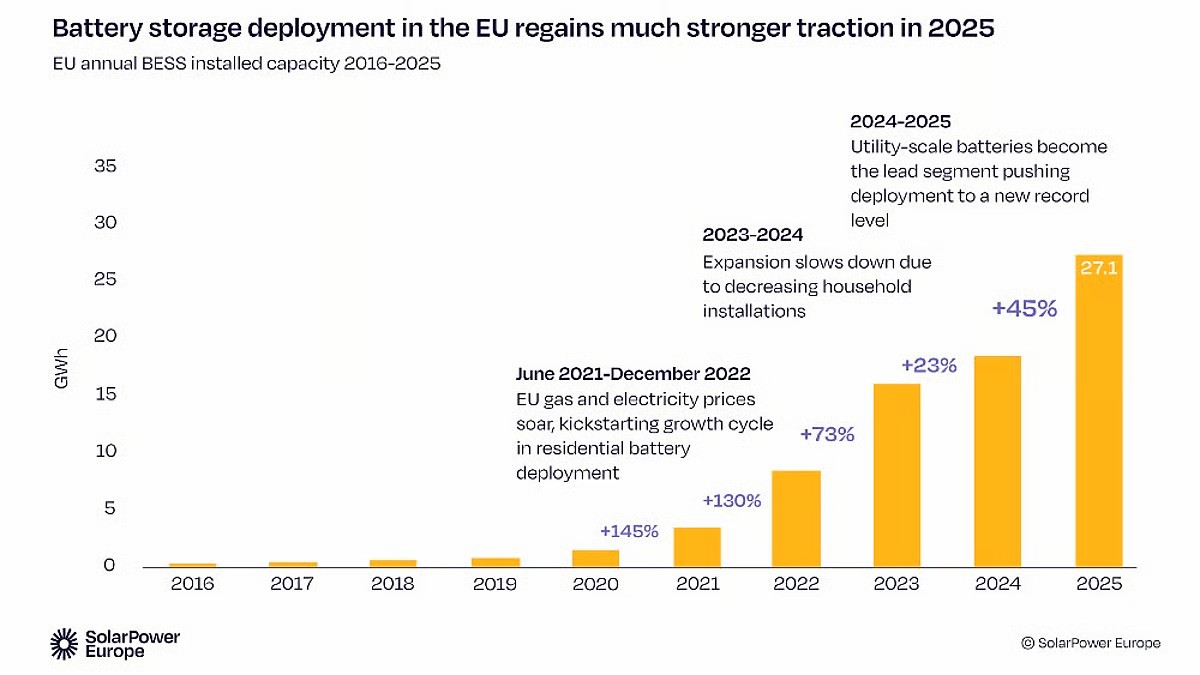

The European Union’s battery energy storage fleet has expanded for the 12th consecutive year, cementing 2025 as yet another record-breaking period for the industry.

According to the latest market review from SolarPower Europe (SPE), the continent deployed 27.1 GWh of new capacity in 2025 alone.

The Power of Utility-Scale

This impressive figure represents a 45% year-on-year growth rate. The surge was primarily powered by the rapid adoption of utility-scale systems across the region.

Large-scale projects have officially emerged as the main driver of this expansion, delivering 55% of all newly added storage capacity this year.

Tenfold Growth Achieved

The report confirms a staggering trajectory: Europe has expanded its battery fleet tenfold since 2021. Total capacity has risen from just 7.8 GWh to a massive 77.3 GWh today.

However, the industry faces a daunting task ahead. To meet energy flexibility needs, the EU must repeat this tenfold increase, scaling to around 750 GWh by 2030.

A Watershed Moment

2025 marked a definitive watershed year for the market. Improved market conditions and strengthened policy frameworks finally allowed large-scale projects to reach these record levels.

“The strong uptake shows investors are ready, the technology is mature, and the system benefits are clear,” noted Walburga Hemetsberger, CEO of SolarPower Europe.

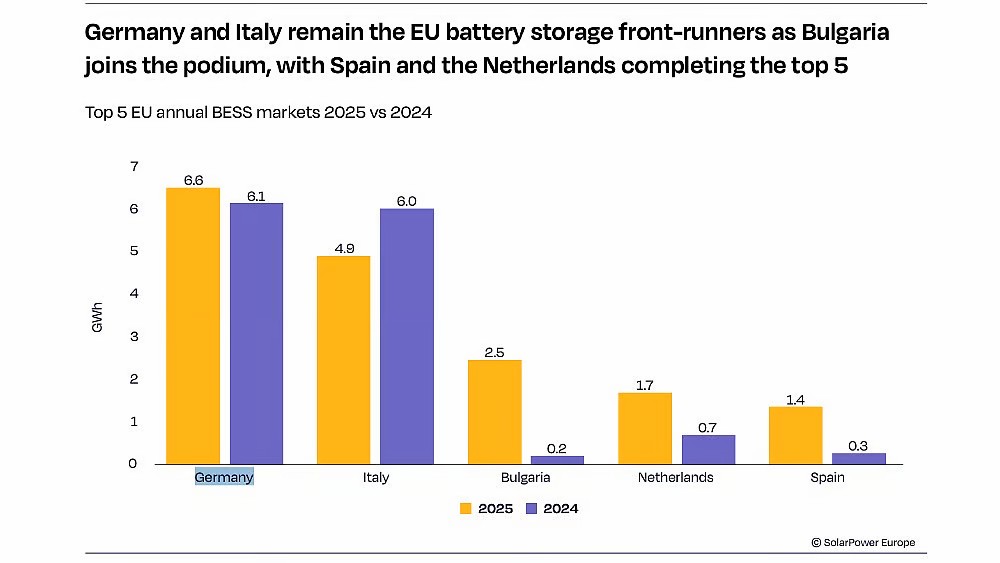

Residential Storage Stalls

In contrast to the utility-scale boom, the residential sector faced headwinds. Residential battery installations declined for the second consecutive year, dropping 6% to 9.8 GWh.

This downturn is largely attributed to lower electricity prices and reduced government support schemes, which have dampened demand from homeowners.

Manufacturing Realities

The report also highlights the state of EU manufacturing. While the region boasts a solid industrial base with 252 GWh of nominal cell production capacity, structural gaps remain.

Crucially, more than 90% of this existing cell capacity is geared toward electric vehicles rather than the stationary storage market needed for grid flexibility.

Supply Chain Gaps

While Europe shows strong capabilities in electrolyte and separator production, the manufacturing of active materials—specifically cathodes and anodes—remains limited.

Project postponements and relatively high production costs continue to challenge competitiveness, underscoring the urgent need for a fully integrated European value chain.

Accelerating Deployment

To keep momentum, SPE identifies three priority areas. First, the EU must accelerate BESS deployment by simplifying permitting processes for both standalone and hybrid projects.

Priority should be given to mature, grid-friendly projects currently stuck in connection queues, while tariff barriers must be addressed to ensure fair market access.

Building Resilience

Second, the report calls for targeted support to build affordable and resilient supply chains. This includes ensuring access to critical raw materials and scaling up recycling capacity.

Developing strategic global partnerships to diversify supply is highlighted as an essential measure to create a cost-effective battery ecosystem.

Focus on Safety and Quality

Finally, the industry must strengthen quality, safety, and sustainability. The report urges the harmonization of EU-wide safety standards and robust incident reporting.

It also recommends enhancing regulations for second-life battery use and implementing mandatory carbon footprint disclosure across the entire value chain.