The U.S. energy storage industry achieved a historic milestone in the second quarter of 2025. According to the latest U.S. Energy Storage Monitor report jointly released by the American Clean Power Association (ACP) and Wood Mackenzie, quarterly installations reached a record-breaking 5.6 GW, marking a new era of rapid growth for the American energy storage market.

Utility-Scale Storage Leads the Charge

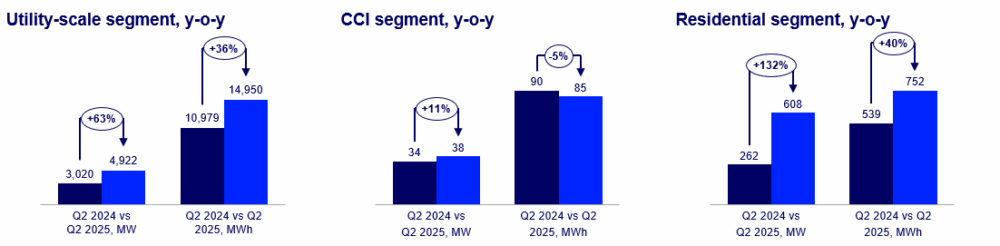

The utility-scale storage market demonstrated particularly robust performance in Q2, with installations reaching 4.9 GW—a single-quarter record. This installed capacity is sufficient to power 3.7 million American homes during average peak demand periods. Notably, the geographic distribution of storage deployment is expanding beyond states that were early adopters.

From a regional perspective, Texas, California, and Arizona maintained their leadership positions, with each state adding over 1 GW of new capacity in the second quarter. These three states have become primary drivers of the U.S. energy storage market, leveraging their abundant renewable energy resources, supportive policy frameworks, and growing electricity demand.

Even more encouraging is the emergence of activity in new markets. The Southwest Power Pool (SPP) region saw renewed activity after a three-year hiatus, with three storage projects coming online in Oklahoma during Q2. Additionally, Florida and Georgia experienced major forecast upgrades due to aggressive procurement by vertically integrated utilities.

Noah Roberts, Vice President of Energy Storage at ACP, stated: “Energy storage is being quickly deployed to strengthen our grid as demand for power surges and is helping to drive down energy prices for American families and businesses. Despite regulatory uncertainty, the drivers for energy storage are strong and the industry is on track to produce enough grid batteries in American factories to supply 100% of domestic demand. Energy storage will be essential to the expansion of the U.S. power grid and American energy production.”

Residential Storage Market Shows Strong Growth

The residential storage market also performed exceptionally well in Q2, adding 608 MW of capacity—a 132% year-over-year increase and an 8% quarter-over-quarter jump. This growth was primarily driven by California, Arizona, and Illinois, where solar-plus-storage attachment rates reached new highs while higher-capacity systems gained market share.

The rapid expansion of the residential storage market reflects consumers’ growing emphasis on energy independence and grid resilience. Particularly after experiencing multiple extreme weather events and power outages, an increasing number of households are choosing to install storage systems as backup power sources while also capturing economic benefits through time-of-use rate arbitrage.

In contrast, the community-scale, commercial and industrial (CCI) storage market experienced more modest growth, adding 38 MW in Q2—an 11% year-over-year increase. California and New York led this segment, accounting for over 70% of total capacity, while Illinois began showing growth momentum. However, community storage deployment remained limited due to high costs and policy constraints.

Policy Uncertainty Presents Challenges

Despite strong market performance, policy uncertainty remains a sword of Damocles hanging over the industry. The report forecasts that U.S. energy storage will reach 87.8 GW by 2029, driven primarily by residential and utility-scale segments. However, due to pending Foreign Entity of Concern (FEOC) regulations on battery cell sourcing, U.S. utility-scale storage installations could drop 10% year-over-year in 2027.

Allison Feeney, research analyst at Wood Mackenzie, noted: “Pricing and FEOC uncertainty and slow community storage development are expected to limit CCI segment growth below 1 GW by 2029, though Massachusetts’ SMART 3.0 may help boost future deployment. Residential storage is expected to outpace solar due to stronger policy resilience, high attachment rates in key markets like California and Puerto Rico, and continued ITC access through third-party ownership.”

Allison Weis, global head of storage at Wood Mackenzie, stated that while the One Big Beautiful Bill Act (OBBBA) preserved the ITC for energy storage, headwinds remain and the five-year buildout could be reduced by 16.5 GW.

Weis explained: “After 2025, utility-scale storage projects must comply with new, stringent battery sourcing requirements to receive the ITC. While domestic cell supply is ramping up, supply chain shortages are possible, although developers are continuing to consider supply from China to fill in any gaps. A rush to start construction under the more certain near-term regulatory framework uplifts the near-term forecast. Projects that have not met certain milestones by the end of 2025 are at risk of exposure to changing regulations. There is additional downside risk if further permitting delays threaten solar and storage projects.”

Supply Chain Localization Accelerates

Facing policy uncertainty, the U.S. energy storage industry is accelerating supply chain localization efforts. Multiple battery manufacturers have announced plans to establish factories in the United States to meet growing domestic demand and comply with potential sourcing requirements. This trend not only helps enhance supply chain resilience but will also create more job opportunities in America.

However, the localization process takes time, and during the transition period, supply chain shortages may become a bottleneck constraining industry development. How to balance supply chain security with sustained market growth will be a critical challenge facing the U.S. energy storage industry in the coming years.

Overall, the U.S. energy storage market is in a period of rapid growth while simultaneously facing multiple challenges related to policy and supply chain issues. Whether the industry can maintain its current growth momentum will largely depend on regulatory clarity and supply chain responsiveness.