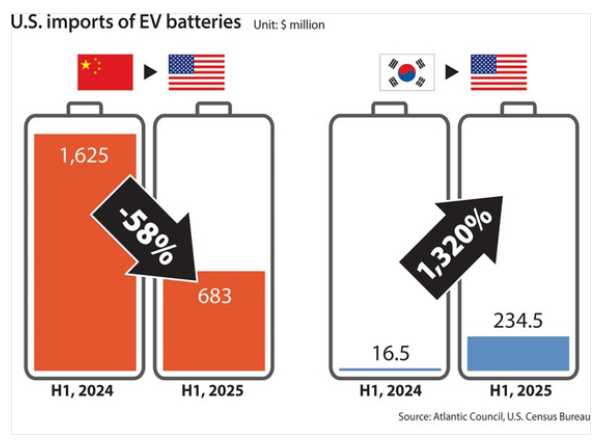

1. U.S. Battery Import Landscape Reaches a Historic Turning Point

In the first half of 2025, U.S. imports of lithium-ion EV batteries from Korea reached $234.5 million, a 1,320% increase year-on-year, and a 2,850% jump compared to the same period in 2023. Over the same period, U.S. imports from China fell by 58% to $683 million. Market share shifted dramatically: China’s share dropped from 72% to 38.1%, while Korea’s surged from 0.73% to 13.1%.

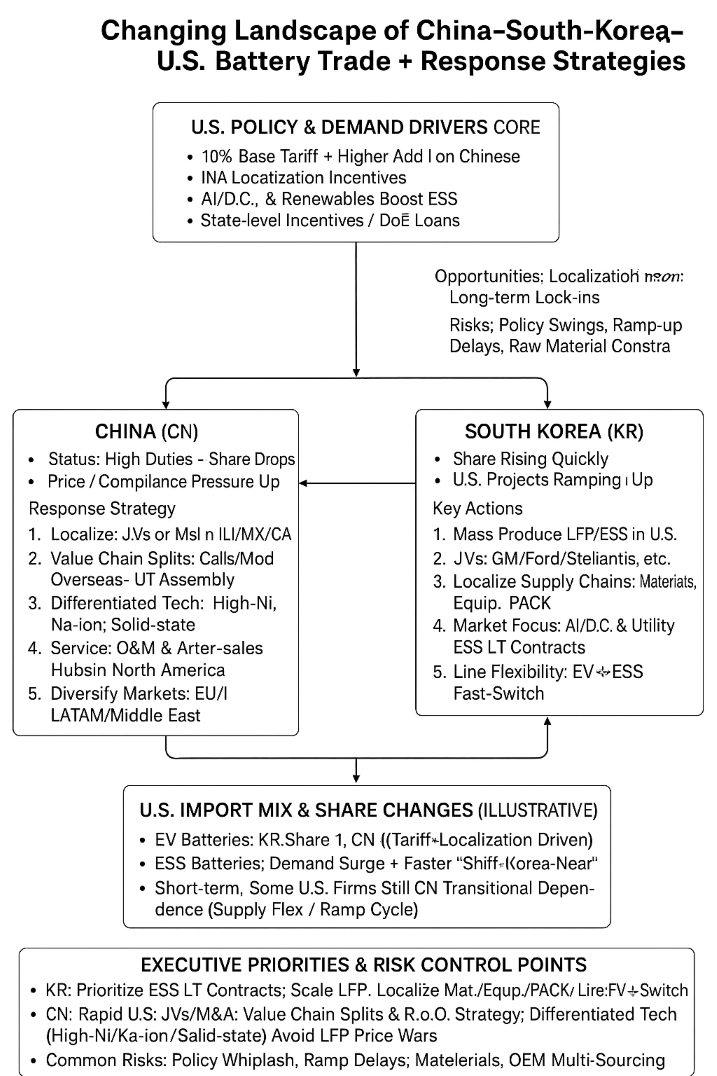

2. Tariff Policy Reshapes the Market: 10% Baseline + Higher Duties on China

From April 2025, the U.S. imposed a 10% “baseline tariff” on battery imports, with significantly higher additional duties on Chinese products.

Currently, Chinese EV batteries face a combined tariff of about 38.4%, and ESS batteries 40.9%, with rates set to rise to 58.4% next year.

This policy greatly increases the landed cost of Chinese batteries, opening a competitive window for Korean producers.

3. Korea’s Big Three Accelerate U.S. Expansion: 600 GWh Capacity Planned

LG Energy Solution (LGES): Three Ultium Cells joint plants with GM total over 130 GWh; its Holland, Michigan plant has begun producing LFP ESS batteries and secured a ~$4.3B ESS order from Tesla.

Samsung SDI: Two 34 GWh plants in Indiana with Stellantis, plus a 27–36 GWh joint plant with GM; plans to use part of its Indiana lines for ESS cell production.

SK On: Two plants in Georgia already in operation; the BlueOval SK joint venture with Ford totals 129 GWh, with some lines to be converted to ESS-dedicated LFP.

Together, these projects could deliver 600 GWh of capacity in the U.S., enough for about 7.5 million high-performance EVs.

4. LFP Technology as Korea’s Winning Card: Cost and Safety Advantages

Under the combined impact of tariffs and IRA localization incentives, lithium iron phosphate (LFP) has emerged as the preferred chemistry for ESS and mid- to low-end EVs thanks to lower cost, longer cycle life, and better thermal stability. LGES, Samsung SDI, and SK On are rapidly scaling LFP production in the U.S. to reduce costs and strengthen competitiveness against Chinese manufacturers.

5. High Tariffs Don’t Mean Zero China: U.S. Firms Still Depend Short-Term

Despite steep tariffs, some U.S. automakers still rely on Chinese batteries in the short term. For example, GM is sourcing from CATL for the new Bolt during a production ramp-up gap. This shows that Chinese supply remains necessary for certain transitional periods.

6. ESS Becomes the Main Growth Battlefield: Driven by AI and Data Centers

The rapid expansion of AI computing centers, data centers, and renewable energy infrastructure is driving explosive ESS demand in the U.S.

In June 2025, U.S. ESS battery imports from Korea reached $243 million, a record high, while Chinese imports fell to $441 million, the lowest since 2022.

The pace of “China-down, Korea-up” in ESS may surpass that of the EV battery sector.

7. Chinese Companies’ Breakthrough Paths: Localization, Technical Differentiation, and Market Diversification

1. Localize Manufacturing in North America

Establish joint ventures or acquire plants in the U.S., Mexico, or Canada to comply with rules of origin and avoid high tariffs; invest in or acquire existing U.S. battery plants for faster entry.

2. Split the Value Chain and Use Transshipment

Produce cells/modules in FTA countries (Mexico, Canada), with final PACK assembly in the U.S.; set up transit manufacturing bases in Southeast Asia to meet origin requirements flexibly.

3. Compete via Technical Differentiation

Focus on high-nickel ternary, sodium-ion, and solid-state batteries to avoid LFP price wars; develop ultra-long-life ESS products for grid and data center use.

4. Build Overseas Brand and Service Capability

Establish O&M and after-sales centers in North America; participate in state-level ESS tenders to gain market share.

5. Diversify Global Markets

Expand aggressively in Europe, Latin America, and the Middle East, leveraging Belt and Road and energy transition projects for large-scale orders.

8. Opportunities and Risks in the China-Korea-U.S. Triangle

Opportunities

- Korea: Policy tailwinds, capacity expansion, ESS market boom

- China: Technology upgrades, cross-border partnerships, non-U.S. market growth

Risks - Policy volatility in tariffs and trade rules

- Ramp-up delays at new plants

- Upstream material supply constraints

- Automakers’ multi-sourcing strategies reducing single-supplier share

9. Strategic Recommendations for the Next Two Years: Tariffs, Localization, and Technology Upgrades

For Korean firms: Keep expanding localized capacity, secure ESS contracts, maintain EV↔ESS production flexibility.

For Chinese firms: Accelerate North American investment, push differentiated technology routes, and strengthen growth in non-U.S. markets to spread policy risk.

Conclusion

Tariff policy is reshaping the global battery trade landscape. Korean firms are gaining ground in the U.S. through localization and LFP technology, while Chinese companies must respond with flexible international layouts and technological differentiation. Over the next two years, ESS and mid- to low-end EV markets will be the main battlegrounds. Those who can balance tariffs, localization, and technological upgrades will be the likely winners in the next round of the global battery industry race.