1. Event Timeline: One Pause Button Disrupts the Whole Chain

AESC halts South Carolina battery cell project. In June, AESC cited “policy and market uncertainty” when it announced a pause on its $1.6 billion battery plant in Florence, South Carolina. The project was originally slated to supply cells for BMW’s US-built EVs. The company reiterated its long-term commitment to investment and job creation.

BMW’s US battery pack and vehicle timelines remain unchanged. BMW still plans to start production at its Woodruff high-voltage battery pack plant in 2026. These packs will go into electric vehicles built at BMW’s Spartanburg (Greer) assembly plant, which is also slated to begin EV production that year.

Importing Chinese cells emerges as a fallback plan. With US cell capacity from AESC now uncertain, reports suggest BMW is considering importing battery cells from China—then assembling them into packs in Woodruff—to safeguard the 2026 start-of-production (SOP) schedule.

Summary: The cell side has stalled, while the pack and vehicle sides proceed as planned. “Temporary imports” are becoming a realistic option to protect launch timelines.

2. Technology Context: Gen-6 Cylindrical Cells Lock in Supply Needs

Neue Klasse will use BMW’s sixth-generation cylindrical cells (46 mm diameter, varying heights), promising +20% energy density, +30% driving range, and +30% faster charging over current prismatic cells, along with an 800 V architecture. This technology is deeply integrated with the vehicle body, thermal management, and battery management systems (BMS), making supplier changes complex.

BMW secured supply from CATL and EVE Energy as early as 2022 for these cells. Whether they come temporarily from China or eventually from North American production, these partners are already embedded in BMW’s technical and quality framework.

3. Why Switching Suppliers Isn’t Simple: From Part Swap to Full Vehicle Revalidation

Even if the chemistry and dimensions remain the same, changing origin, production line, equipment, or process parameters triggers additional validation. OEMs must re-check cell consistency, durability, thermal safety, NVH, and battery state-of-health algorithms, as well as re-map BMS parameters, pack design margins, and thermal/fast-charge limits.

Comprehensive revalidation can take 12–18 months, leaving little margin against the 2026 launch window. Hence the logic of “temporary imports with minimal technical change” to reduce validation scope.

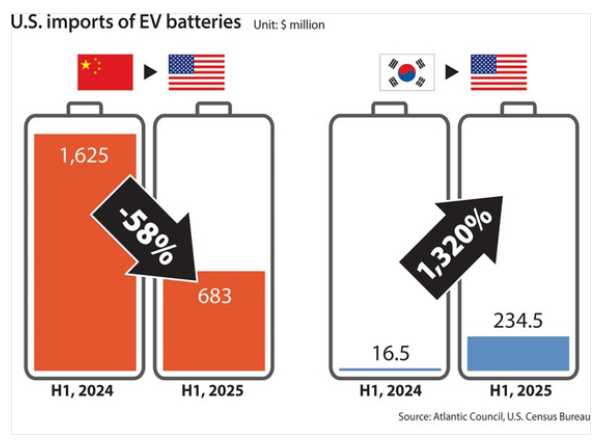

4. Tariffs and Compliance: Buying Time Now, Paying Later

Effective tariffs could reach ~82%. Combined Section 301 and other duties on Chinese-made lithium-ion batteries are projected to reach effective rates of around 82% by 2026. Temporary imports may preserve timelines but would significantly increase unit costs.

Policy volatility is itself a cost. Rising tariffs and shifting US tax incentive rules have slowed or halted multiple battery and clean energy projects, contributing to AESC’s pause.

5. Production Schedule Constraints

Global rollout: Debrecen, Hungary comes online first in 2025; Spartanburg follows in 2026 with EV production. This leaves limited buffer for revalidation on the US side.

Plant integration: Woodruff assembles battery packs. Even with imported Chinese cells, pack assembly, end-of-line testing, and functional safety validation must adapt to the new supply source.

6. Industry-Wide Impact: BMW Isn’t Alone

Automakers slowing down. GM has reduced its planned US battery plants from four to three and shifted some lines toward LFP chemistries. Ford has delayed certain projects to 2027–2028, signaling more cautious capital spending.

More cancellations and delays. Think tank data show over $14 billion worth of US clean energy and battery projects delayed or scrapped since 2025, underlining the “hidden tax” of policy uncertainty.

7. Three Strategic Paths: Balancing Cost, Time, and Compliance

- Short-term fix: Import Chinese cells + assemble locally (minimal changes)

- Pros: Maximizes reuse of existing chemistry and validation data; minimizes revalidation scope; protects 2026 SOP.

- Cons: Steep tariff/logistics costs; still exposed to future policy shifts.

- Mid-term transition: Accelerate North American localization with existing partners

- Approach: Restart AESC’s US projects or bring in other partners to build/expand lines in North America using the same chemistry and structure.

- Challenges: Construction and equipment lead times, plus production and quality ramp-up, could still clash with the 2026–2027 production window.

- Regional arbitrage: Mexico/Canada local production using Chinese technology

- Logic: Building within the USMCA trade zone could ease tariff/compliance pressures while keeping technology aligned with CATL/EVE.

- Conditions: Must meet origin and “foreign entity of concern” rules to avoid policy blowback.

8. Three Takeaways for Chinese Battery and Material Companies

- Technology equation before geography equation. OEM demand for Gen-6 cylindricals locks in material system requirements (high-nickel/NMX, fast-charge electrolyte, graphite/silicon-carbon anodes) with 800 V compatibility as the key to orders.

- North American compliance as “second productivity.” Beyond joint validation, suppliers must build capabilities in origin documentation, supply chain traceability, and third-party audits to quantify and manage IRA/tariff/FEOC risks.

- Portfolio flexibility. In an OEM slowdown cycle, offering both LFP/LMFP and high-nickel products enables cost–performance switches across platforms.

9. Risk Checklist for Investors and Operators (2025–2027)

- Policy milestones: 2024–2026 tariff changes and battery-related incentives directly determine the economic viability of imports.

- AESC project progress: Financing, equipment procurement, and ramp-up schedules at South Carolina and Kentucky sites are key to medium-term local supply.

- BMW global production shifts: The Hungary–Germany–US rollout sequence defines US revalidation windows and risk buffers.

Conclusion: Buying Back Time Amid Uncertainty

AESC’s “pause button” on South Carolina cells is a supply chain shock for BMW’s North American battery plans, but vehicle and pack production schedules still point to 2026. In the short term, importing Chinese cells for local pack assembly looks like the lowest-risk path. In the long term, North American localization remains the only sustainable answer for cost and compliance. Between the platform benefits of Gen-6 cylindricals and the unpredictability of trade policy, BMW and its partners must make the smallest technical changes possible to buy the greatest certainty of on-time launch.