The global lithium market is facing a paradox. Prices have plunged, investment is slowing, and producers are hurting—yet the underlying demand story remains undeniably strong.

In June 2024, Reuters reported that lithium hydroxide prices have fallen by a staggering 90% from their record highs in 2022. This collapse has sent shockwaves across the battery materials industry, squeezing margins to zero or even negative for many producers. Even industry giants like Albemarle, the world’s largest lithium producer, have been forced to cut costs and delay new projects in response to the downturn.

Yet in the face of this bleak short-term outlook, mining major Rio Tinto is doing the opposite. The company recently made a bold strategic move by acquiring U.S.-based Arcadium for $6.7 billion, and announced partnerships with Chilean state entities to develop two major lithium projects.

Rio’s contrarian stance is a powerful signal that the current price crash may be just a bump in the road for what it sees as a multi-decade supercycle in lithium demand.

A Brutal Market for Lithium Producers

For most lithium producers, 2024 has been financially painful. Prices of lithium hydroxide—crucial for high-performance electric vehicle (EV) batteries—have collapsed as new supply continues to flood the market. This oversupply has driven average selling prices down to levels where operating profits are nonexistent or negative.

According to Wood Mackenzie, multiple producers are now running at break-even or worse. Projects that were once expected to drive profits are now being mothballed or postponed.

In many ways, this correction is a textbook case of lithium oversupply. Encouraged by sky-high prices in 2021 and 2022, dozens of mining firms rushed to bring new capacity online. As a result, global lithium production expanded by over 35% year-on-year in 2024, according to the International Energy Agency (IEA).

This flood of new material—combined with slower-than-expected buying from battery manufacturers due to inventory overhangs—has caused a dramatic supply-demand mismatch.

Demand is Strong, But Hidden Under the Surface

Beneath the headline-grabbing price collapse, a different story is unfolding. Despite oversupply concerns, global lithium demand is actually booming.

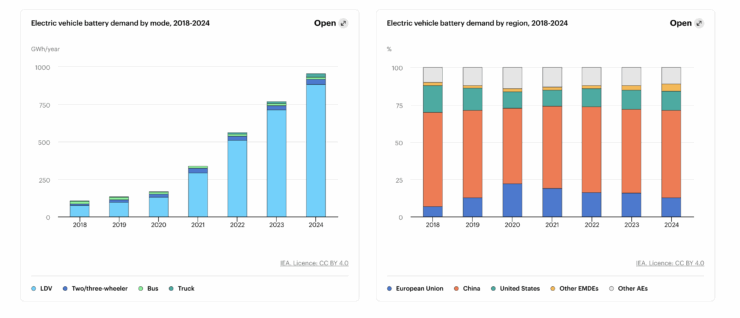

The IEA estimates that lithium usage grew by 30% in 2023, a number that mirrors the entire size of the global market just six years earlier in 2018. This is not a market in decline—it’s a market experiencing structural transformation.

The biggest driver, unsurprisingly, remains electric vehicles. Sales of new energy vehicles rose by 25% in 2023 and were up another 29% in Q1 of 2024, according to consultancy Rho Motion. Every EV requires a lithium-ion battery, and as vehicles become larger and offer longer ranges, the electric vehicle battery demand per unit is increasing.

But there’s another major force at play: energy storage systems (ESS). As the world’s energy mix shifts toward intermittent renewable sources like solar and wind, storage becomes essential. Lithium-ion batteries are currently the most scalable and widely deployed solution for this need.

These two sectors—EVs and ESS—are poised to drive exponential demand for lithium, despite the cyclical nature of commodity pricing.

Rio Tinto’s Contrarian Bet

In a market where most producers are pulling back, Rio Tinto stands out.

The global mining firm, better known for its iron ore and copper operations, has made it clear that it views lithium as a critical strategic commodity. By acquiring Arcadium, Rio not only gains access to significant U.S.-based production capacity, but also strengthens its foothold in a key Western market where domestic battery supply chains are becoming politically prioritized.

Furthermore, Rio is partnering with Chilean state-owned entities to develop two new projects. This is particularly notable given the geopolitical sensitivity and regulatory complexity of Chile’s lithium industry, which accounts for nearly one-third of global supply.

By pursuing these deals, Rio Tinto is signaling its long-term confidence in lithium’s role in the clean energy transition. In its latest statement, the company forecasted that lithium demand will grow at a compound annual rate (CAGR) of over 10% through 2040—more than tripling the size of the current market.

This is not just a resource play; it’s a strategic positioning for dominance in what many analysts see as the most important metal for the 21st century.

Structural Supercycle or Boom-and-Bust?

The debate over lithium’s future now centers on whether we are witnessing a short-term correction or the beginning of a longer downturn. Bulls argue that the current glut is temporary—driven by supply chain timing mismatches—and that battery demand will soon catch up and flip the market back into deficit.

Bears, meanwhile, warn that alternative battery chemistries (such as sodium-ion and solid-state batteries) could eventually reduce the world’s dependence on lithium, particularly for lower-end applications.

However, these alternatives are still far from commercialization at scale, and lithium remains unmatched in terms of energy density, recyclability, and infrastructure compatibility. For now, lithium remains the only viable option for high-performance EVs and scalable grid storage.

A More Resilient Lithium Market Emerging?

Several signs suggest that the lithium market may be heading for a rebalancing:

- Project Delays: Companies are slowing investment, which could restrain future supply growth.

- Inventory Drawdowns: Battery makers are beginning to draw down existing inventory, increasing purchasing activity.

- Policy Support: Government mandates around EV adoption and grid storage are becoming more stringent, locking in baseline demand.

- Cost Curve Compression: High-cost producers are being squeezed out, which will gradually rebalance the market toward more efficient players.

If demand continues its trajectory—and if even a modest portion of delayed EV and storage growth resumes in 2025—the current lithium price collapse could prove short-lived.

Conclusion: The Long Game

The lithium market is currently caught between two forces: short-term oversupply and long-term structural demand growth.

For producers and investors, the challenge is to weather today’s volatility while preparing for tomorrow’s boom. For industry giants like Rio Tinto, that means betting now while assets are undervalued, regulatory frameworks are evolving, and long-term demand drivers remain intact.

Whether this strategy proves prescient or premature will depend on how quickly the market absorbs its current surplus. But if lithium maintains its place at the heart of the clean energy transition—as most experts expect—it’s likely that the smart money is playing the long game.