The global battery supply chain is a critical component of the electric vehicle (EV) revolution, and China has emerged as the dominant player in this industry. A recent study by researchers from Fraunhofer FFB and the University of Münster highlights China’s supremacy in the lithium-ion battery supply chain, from raw material extraction to battery production. The findings underscore the vulnerability of regions like Europe, which are heavily dependent on China for critical minerals and battery technologies.

1. The Dominance of China in the Battery Supply Chain

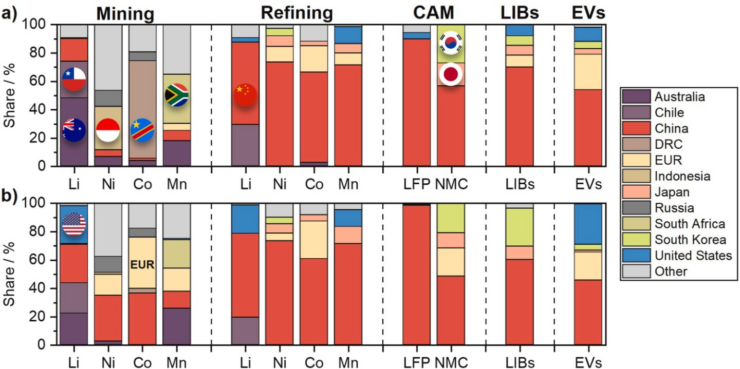

The study conducted by Fraunhofer FFB and the University of Münster provides a detailed analysis of the ownership structures behind mines, refineries, and production facilities across the global battery supply chain. The findings reveal that China dominates almost every stage of lithium-ion battery production, from raw material extraction to the final assembly of batteries for electric vehicles.

China’s control extends to key materials such as lithium, nickel, cobalt, and manganese, which are essential for producing cathodes in lithium-ion batteries. While Europe leads in terms of EV production, its reliance on Chinese supply chains makes it vulnerable to geopolitical tensions and export restrictions. Professor Simon Lux, Director of Fraunhofer FFB, warns that this dependency could lead to massive economic losses if China were to impose export restrictions during a geopolitical conflict.

2. The Geopolitical Tensions Surrounding Raw Materials

The study emphasizes the critical role of raw materials in the battery supply chain. Europe is almost entirely dependent on imports for minerals like lithium and cobalt, which are sourced from regions such as Australia, Chile, and the Democratic Republic of the Congo (DRC). However, Chinese companies hold significant shares in these mining operations, further cementing China’s dominance.

For example, 74% of global lithium production comes from Australia and Chile, but Chinese companies own 29% of the production capacity, while U.S. companies account for an additional 26%. In contrast, Europe has no significant shares in foreign lithium mines, highlighting its vulnerability to external supply chain disruptions.

The concentration of cobalt production is even more alarming. The DRC produces over 70% of the world’s cobalt, and Chinese companies dominate the refining and processing of this critical material. This dominance raises concerns about the long-term sustainability of Europe’s EV industry if China were to restrict access to these raw materials.

3. Opportunities for Reducing Dependency on China

While China’s dominance poses significant challenges, there are opportunities for Europe and the United States to reduce their dependency on Chinese supply chains. One approach is to invest in the expansion of domestic refining capacities. By building more refineries within Europe and the U.S., these regions can process raw materials locally, reducing their reliance on Chinese facilities.

Another strategy is to promote strategic partnerships with countries that have significant mineral reserves, such as Australia, Indonesia, and the DRC. These partnerships could help secure long-term supplies of critical minerals while fostering geopolitical stability in key mining regions.

Additionally, strengthening the circular economy for batteries can help reduce dependency on raw materials from China. By recycling end-of-life batteries and extracting valuable metals like cobalt and lithium from discarded batteries, Europe and the U.S. can reduce their reliance on new raw material extraction.

4. The Future of the Battery Supply Chain

The study highlights the need for a more diversified and resilient battery supply chain to support the global EV revolution. As countries race to meet their climate goals and reduce greenhouse gas emissions, the demand for electric vehicles is expected to grow exponentially. This growth will require significant investments in battery production capacity, raw material extraction, and recycling infrastructure.

China’s current dominance in the battery supply chain underscores the importance of addressing these challenges now. By taking proactive steps to diversify supply chains and invest in local production capabilities, Europe and the U.S. can reduce their vulnerability to external disruptions and ensure a sustainable future for the electric vehicle industry.

In conclusion, the global battery supply chain is at a crossroads. While China’s dominance poses significant challenges, it also presents opportunities for innovation and collaboration. The findings of this study serve as a wake-up call for regions like Europe and the U.S., highlighting the need to act now to secure their place in the EV revolution.