The lithium industry is experiencing another major shockwave! On September 10th, news regarding the imminent resumption of CATL’s Yichun Jiangxiawowo lithium mine operation sent ripples throughout the lithium battery supply chain. While the mine has not officially resumed production, the faster-than-expected progress of resumption plans has already profoundly impacted the lithium carbonate market.

Futures and Spot Markets Hit Hard

In the futures market, lithium carbonate main contracts opened at 69,000 yuan per ton on September 10th, just one step away from the daily limit down price of 68,400 yuan per ton. Despite some intraday recovery, the decline still reached 4.87% by market close. Other lithium carbonate contracts also experienced similar significant drops.

The spot market faced equal pressure. According to Shanghai Steel Union data, battery-grade lithium carbonate prices in the morning session fell 1,500 yuan from the previous day, averaging 72,000 yuan per ton. Shanghai Metals Market’s latest quotation showed that lithium carbonate prices dropped 170 yuan to 74,600 yuan per ton on September 8th, marking the 13th consecutive day of decline.

A-Share Lithium Sector Collectively Declines

The stock market reaction was equally dramatic. On September 10th, lithium industry listed companies saw significant share price drops. The “lithium industry twin giants” Tianqi Lithium and Ganfeng Lithium both opened nearly 5% lower. By market close, Tianqi Lithium fell 5% while Ganfeng Lithium dropped 3.78%, with the entire lithium sector showing collective decline.

Resumption Plans Exceed Expectations

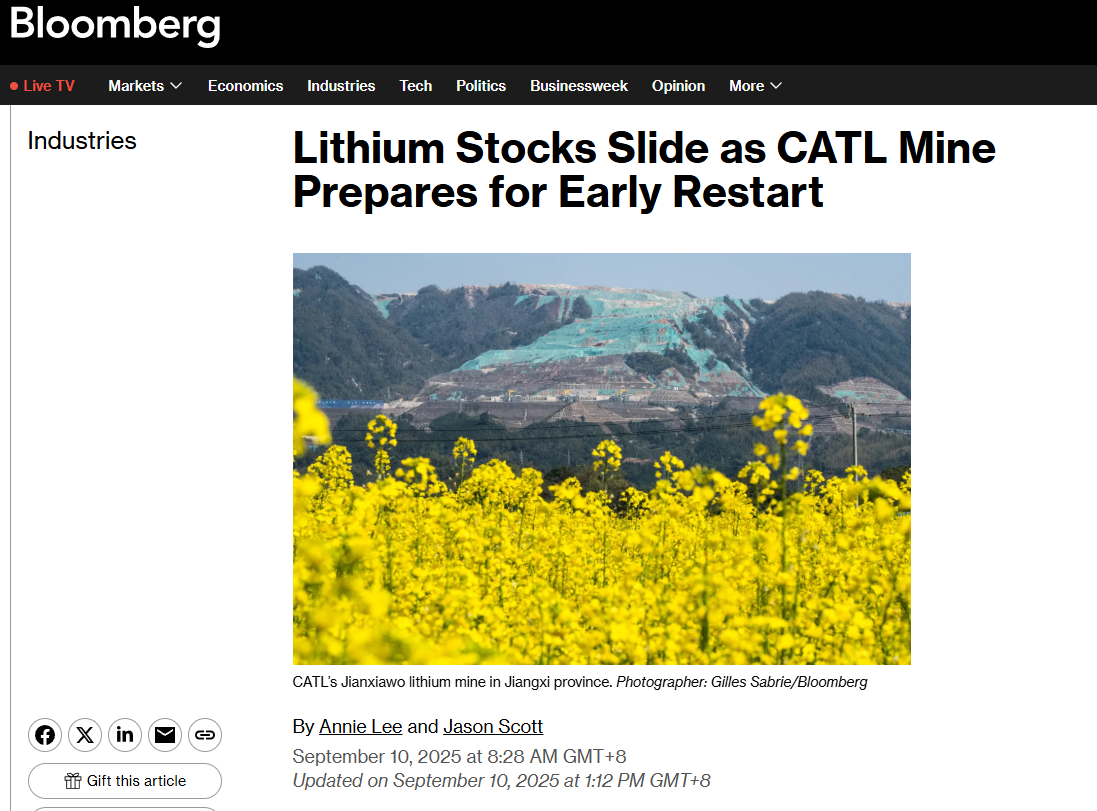

According to Securities Times reporters, on the morning of September 9th, CATL’s controlling subsidiary Yichun Times New Energy Mining Co., Ltd. (Yichun Times) convened a “Jiangxiawowo Lithium Mine Resumption Work Meeting” to specifically advance the mine’s resumption efforts. Sources revealed that CATL’s Jiangxiawowo lithium mine applications for mining rights certificates and mining permits are progressing smoothly, much faster than market expectations, with production resumption expected soon.

The meeting, chaired by Yichun Times’ general manager, made two critical decisions: immediately recall the first batch of original mining area employees who had been reassigned to battery factories, and halt the reassignment of the second batch of employees. To advance the Jiangxiawowo lithium mine resumption work, Yichun Times has established a dedicated working group specifically responsible for this effort.

Massive Mining Area with Far-Reaching Impact

The Jiangxiawowo mining area is currently the largest lithium mica mining area in the Yichun region. According to assessment reports previously disclosed by Yichun Natural Resources Bureau, the mine’s evaluated design project construction investment totals 21.58 billion yuan, with recoverable reserves of 775 million tons in the Jiangxiawowo mining area. Based on a production scale of 30 million tons per year, the mine service life is calculated at 25.83 years.

The mining area’s mining rights began on August 9, 2022, and were originally set to expire on August 9, 2025. Due to mining rights renewal issues, the mining area shut down precisely at 24:00 on August 9, 2025. CATL successfully bid for the area’s exploration rights in April 2022 with an offer of 865 million yuan. The inferred porcelain stone mineral resources are estimated at 960 million tons, with associated lithium oxide resources of 2.6568 million tons, equivalent to approximately 6.57 million tons of lithium carbonate, making it one of the world’s largest single lithium mica mines at the time.

Market Participants Call It “Beyond Expectations”

Regarding the news of CATL’s Jiangxiawowo mining area’s imminent resumption, Securities Times reporters contacted multiple industry and institutional sources, who unanimously described it as “beyond expectations,” with some even calling it “unlikely.”

A representative from a Yichun lithium mining company stated: “From a procedural standpoint, each step requires time, so it doesn’t feel this fast. The news of Jiangxiawowo lithium mine’s imminent resumption won’t have a major impact on fundamentals in the near term; it’s more about emotional and expectational influence.”

A non-ferrous metals researcher from a Shanghai brokerage firm believes that CATL’s Jiangxiawowo lithium mine resumption work meeting not only signifies that resumption timing far exceeds previous market expectations for the Jiangxiawowo mining area itself, but also indicates that the reserve compilation work for the other seven lithium companies in Yichun won’t face significant difficulties. Previously, a considerable portion of market participants believed that besides the Jiangxiawowo lithium mine, the other seven lithium companies in the Yichun region also faced potential shutdowns after September 30th.

Supply Disruption Eases, Return to Fundamental Logic

A senior researcher from a futures company stated: “This means that after supply disruptions temporarily subside, the market will return to fundamental logic. News of Jiangxiawowo lithium mine resumption will significantly weaken market concerns about supply risks, returning to fundamental trading. It’s worth noting that corporate hedging will make supply price-insensitive in the short term; price declines won’t immediately bring supply contraction. Spodumene processing volumes are expected to maintain high levels until year-end, and after substantial resumption of Jiangxiawowo lithium mine, the balance sheet will change.”

Jack He, senior researcher in new energy at Huachuang Securities, pointed out that on the supply side, gradual mine resumptions have reduced market expectations of widespread mine shutdowns. On the demand side, if downstream battery manufacturers plan to rush installations before year-end, they should start stockpiling in late August to September. However, current actual conditions show that battery manufacturers have insufficient willingness and weak intensity for rush installations, with lithium carbonate downstream demand performing below expectations.

Price Decline Trend Continues

Analysts point out that although CATL’s Jiangxiawowo project experienced brief shutdown, the lithium carbonate supply side shows no obvious volume reduction signs. Instead, increased spodumene imports have led to inventory accumulation, contributing to lithium carbonate price declines to some extent.

Statistics show the mining area’s 2025 production is expected at 80,000 tons. If resumption proceeds smoothly, it will significantly impact lithium carbonate fundamentals. Regarding lithium carbonate prices, Shanghai Metals Market’s latest quotation shows lithium carbonate prices fell 170 yuan to 74,600 yuan per ton on September 8th, declining for 13 consecutive days with cumulative 5-day drops of 3,730 yuan. Lithium hydroxide prices also dropped 220 yuan to 75,300 yuan per ton, declining for 13 consecutive days with cumulative 5-day drops of 1,280 yuan.

Historical Review and Outlook

Reviewing previous market trends, since August 10th when CATL’s Jiangxiawowo mining area mining operations stopped, messages indicated the mining area had no short-term resumption plans. On August 11th, CATL responded on the Shenzhen Stock Exchange’s interactive platform that the company had suspended mining operations after the Yichun project’s mining permit expired on August 9th, and was expediting mining certificate renewal applications according to relevant regulations. This news caused lithium carbonate futures to hit daily limits across all contracts, with main contracts rising 8% to 81,000 yuan per ton. By August 18th, lithium carbonate futures prices nearly approached the 90,000 yuan per ton threshold.

Previously, markets expected Jiangxiawowo mine shutdown duration of 3-6 months, with some institutions predicting even longer shutdowns. Now, CATL’s Jiangxiawowo mine has begun planning resumption, with restart timing much faster than previous market expectations. This news confirmation marks the gradual easing of supply-side concerns that have troubled the lithium battery supply chain for months.

In recent years, lithium carbonate prices have experienced enormous volatility. In 2020, lithium carbonate prices hit lows of just 40,000 yuan per ton. Benefiting from rapid domestic new energy vehicle industry development, prices surged continuously, reaching historical highs of 600,000 yuan per ton in 2022, before entering a downward trend and currently hovering around 70,000 yuan per ton.

From a long-term perspective, with continued development of new energy vehicle and energy storage markets, the lithium battery industry still has enormous growth potential. According to GGII data, in the first half of this year, the lithium battery supply chain overall achieved year-over-year growth exceeding 40%. In the battery segment, first-half shipments reached 776 GWh, up 68% year-over-year. Energy storage lithium batteries, boosted by “export rush” effects driving demand, shipped 265 GWh, surging 128% year-over-year.

Industry insiders generally believe that as supply-side disruption factors gradually eliminate, the lithium carbonate market will return to supply-demand fundamental logic. In the short term, markets still need to monitor substantial resumption progress of CATL’s Jiangxiawowo lithium mine and completion of reserve compilation work by other lithium companies in the Yichun region, as these factors will continue influencing lithium carbonate price trends.