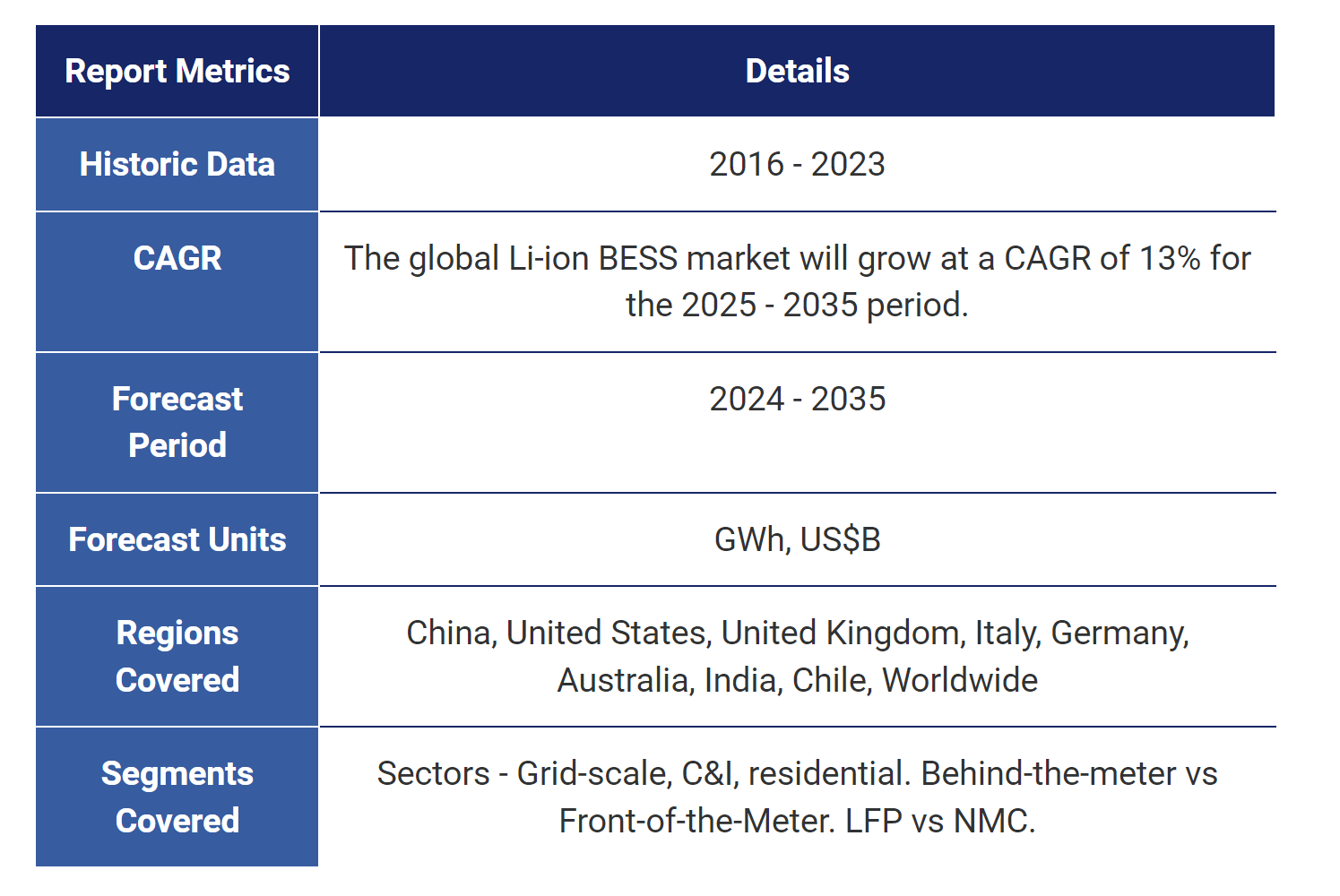

The demand for battery storage solutions is surging as renewable energy sources (RES) increasingly penetrate electricity grids worldwide. Governments and states are rolling out incentives and targets to promote the growth of battery storage systems, accelerating the shift toward sustainable energy. According to a recent report by IDTechEx, the global market for lithium-ion battery energy storage systems (BESS) is projected to reach $109 billion by 2035, with over 4.4 terawatt-hours (TWh) of cumulative installed capacity.

Lithium-Ion Batteries: Dominating the Market

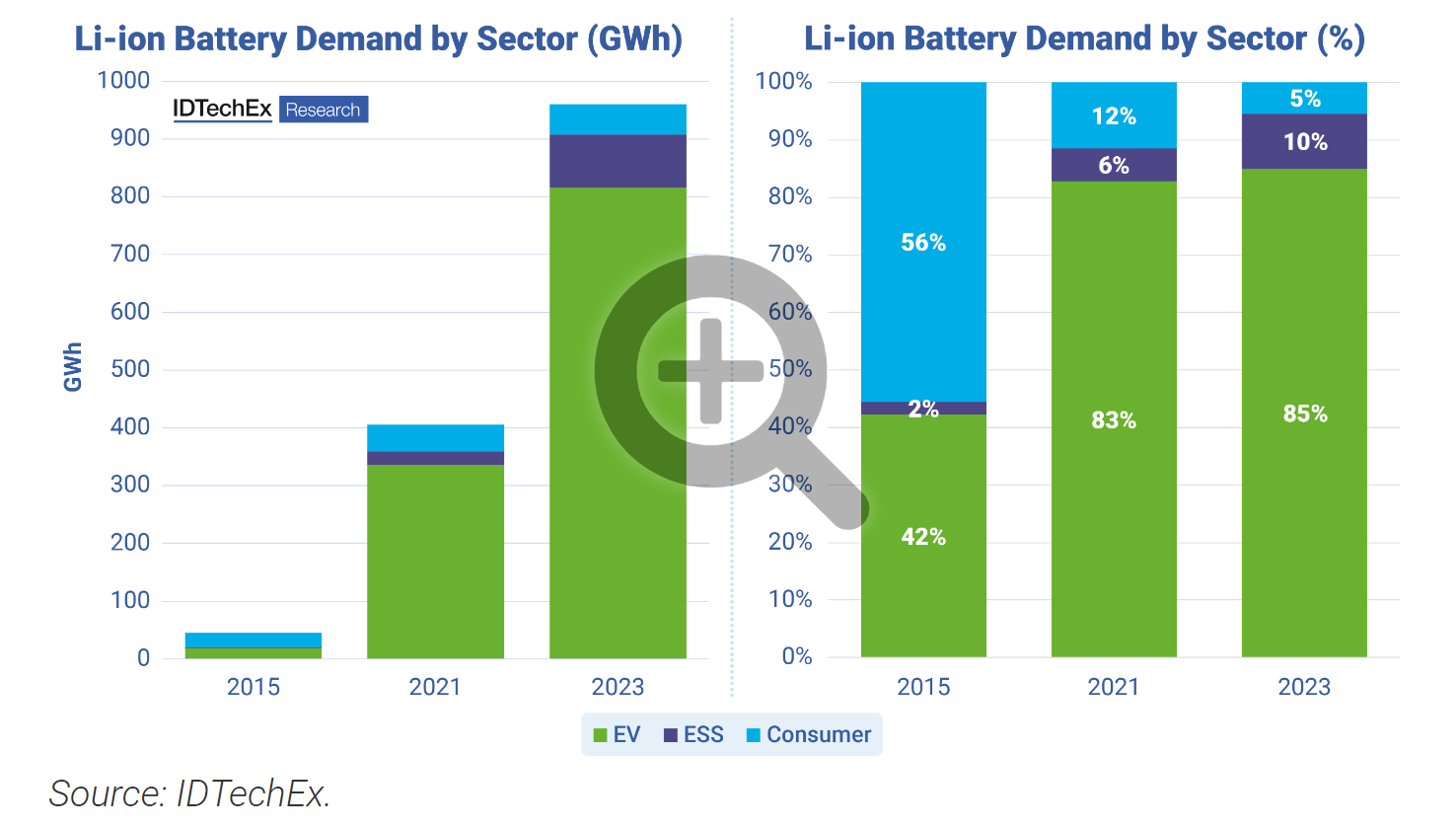

Lithium-ion batteries (LIBs) have become the dominant technology for energy storage, accounting for over 90% of global electrochemical BESS installations. This dominance is primarily driven by their high performance and rapid cost reductions in recent years, largely due to increased demand in the electric vehicle (EV) sector. In 2023, global lithium-ion battery demand reached 960 gigawatt-hours (GWh), a substantial increase from 400 GWh in 2021. While the EV sector continues to dominate demand, the share of lithium-ion batteries for stationary energy storage is steadily increasing.

Emerging Battery Technologies and Safety Innovations

Despite lithium-ion batteries’ current market leadership, other energy storage technologies are vying for market share. These include sodium-ion (Na-ion) batteries, redox flow batteries (RFB), and metal-air batteries. These alternative technologies offer advantages such as the use of more abundant materials, which could help lower costs. However, lithium-ion batteries are expected to maintain their dominance in the medium term, particularly as manufacturers continue to innovate in safety features and energy density.

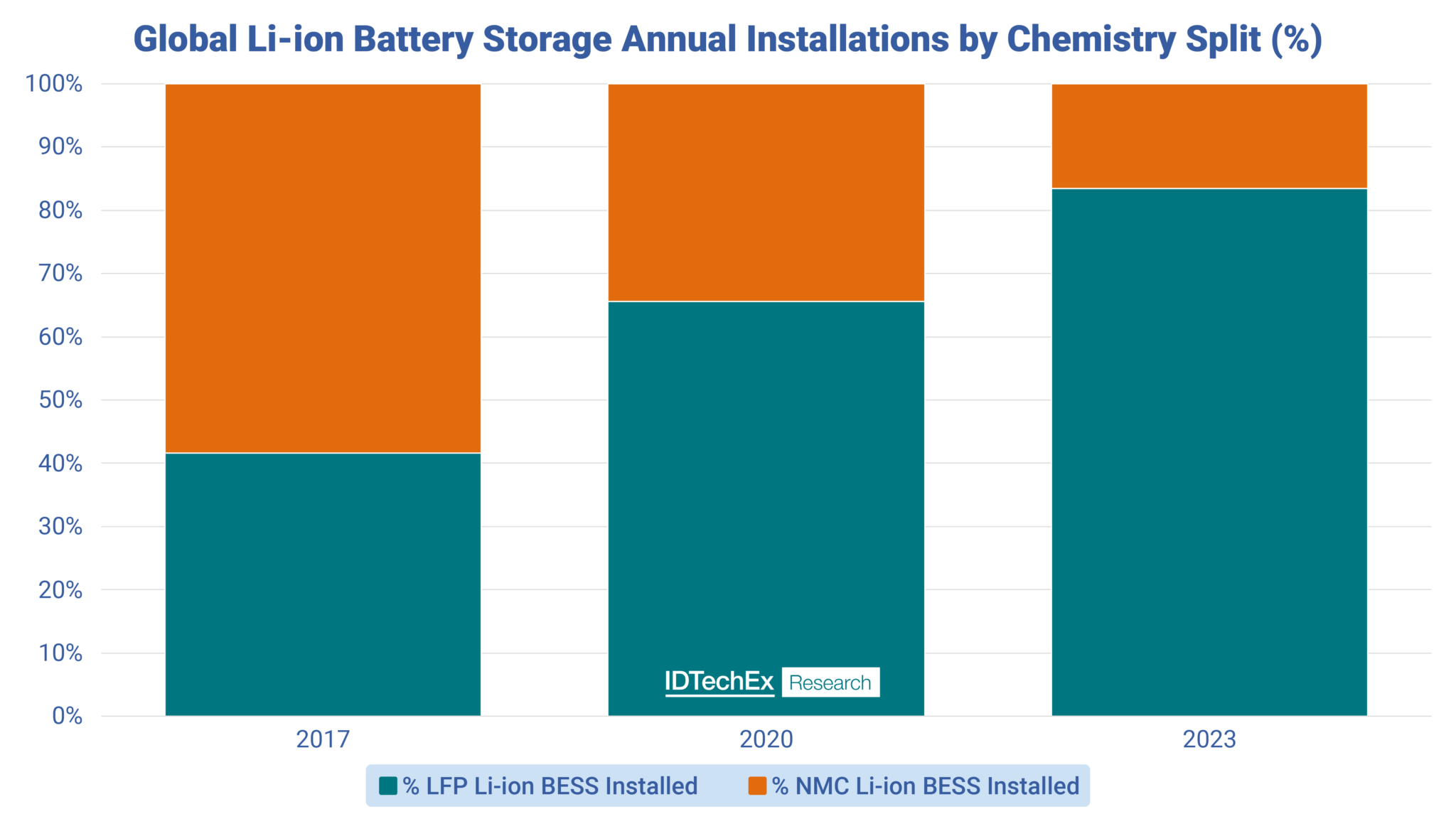

Safety remains a critical issue for lithium-ion BESS, with failures often linked to poor installations, design flaws, or the system operating outside its specifications. The choice of cell chemistry, such as lithium iron phosphate (LFP) versus nickel manganese cobalt (NMC), also impacts safety. While LFP cells generally exhibit better thermal stability, they can pose hazards if thermal runaway occurs. Manufacturers are increasingly implementing technologies like forced air or liquid cooling systems to mitigate safety risks.

Growing Adoption of Large-Scale Energy Storage

LFP batteries are gaining popularity due to their lower cost and longer cycle life. To address concerns about lower energy density compared to NMC cells, many Chinese BESS manufacturers have developed large cell formats, allowing for the deployment of containerized BESS systems with capacities exceeding 5 MWh. These systems are designed to maximize space utilization within containers, reducing installation costs and spatial footprints for large-scale projects.

The Role of the U.S. and China in BESS Growth

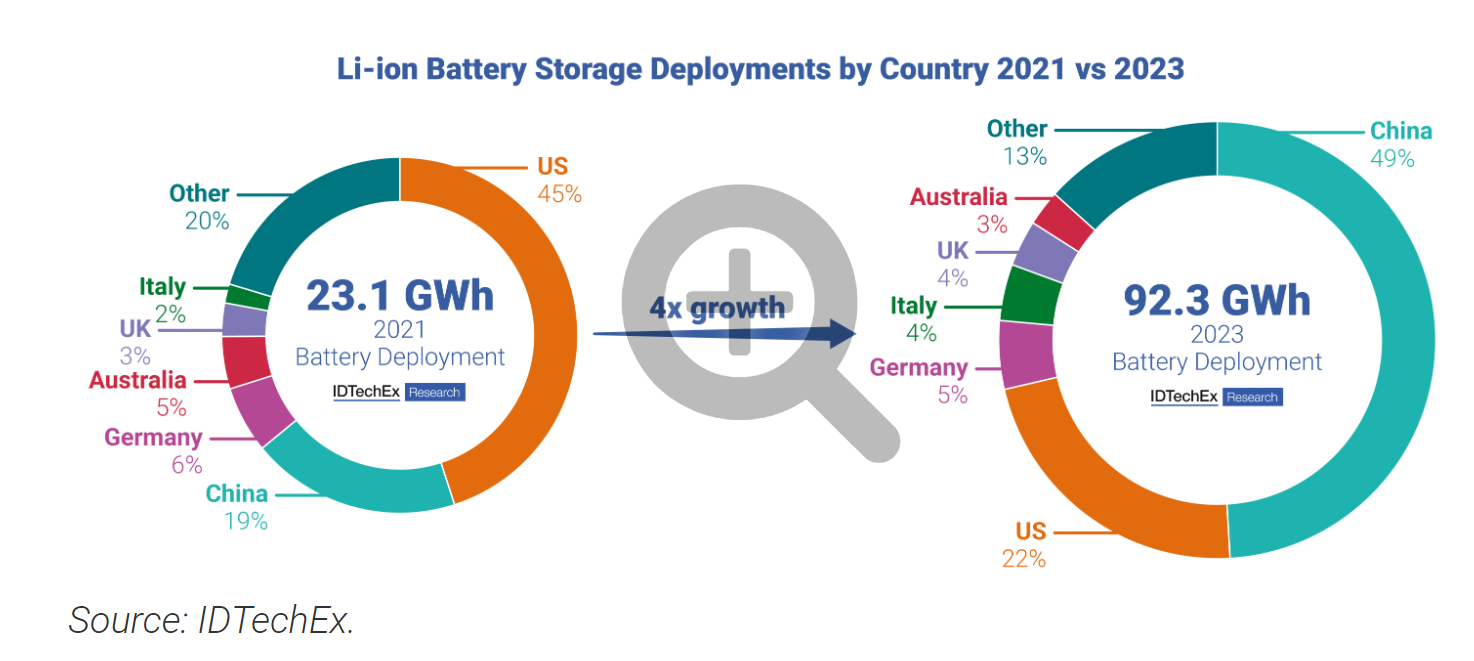

In 2023, China and the U.S. accounted for 71% of the global 92.3 GWh of lithium-ion BESS installations. As leading players in the global energy storage market, both countries are setting the pace for future growth. However, other nations like Germany, Australia, and Chile are also expected to show strong growth in the coming decade. Government incentives, such as the Capacity Investment Scheme in Australia and India’s Viability Gap Funding, will be key drivers of this expansion.

IDTechEx’s report also highlights that U.S. companies are ramping up their domestic manufacturing capabilities to take advantage of tax incentives introduced under the Inflation Reduction Act. By building localized supply chains, these companies aim to reduce production costs and compete more effectively in the global market.

Conclusion

The lithium-ion battery energy storage market is set for explosive growth, driven by technological innovation, government incentives, and the increasing integration of renewable energy sources into power grids. While alternative battery technologies are emerging, lithium-ion BESS is expected to dominate the market in the near future, reaching a value of $109 billion by 2035.