The Energy Bottleneck: Choking the AI Boom

Foley & Lardner LLP released its 2026 Data Center Development Report today, sounding a critical alarm for an industry driven by the explosive growth of AI and Large Language Models (LLMs). Despite soaring market demand, the report highlights that physical power supply has become the ultimate choke point.

The survey results are stark: 54% of respondents identified “energy availability and redundancy” as the single greatest obstacle to successful development between now and 2030. This figure far outweighs other challenges, signaling that the industry’s primary focus has shifted from expanding computing capacity to securing the underlying electricity.

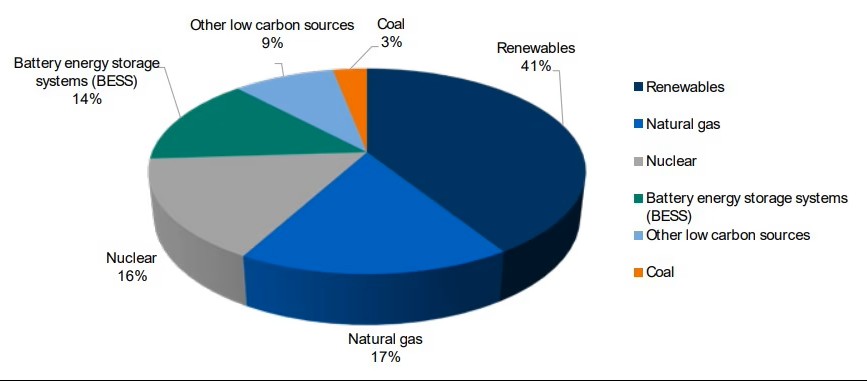

The Ideal Mix: Renewables Lead, Storage Follows

The industry has reached a consensus on the “ideal energy mix” needed to quench this power thirst. According to the survey data (as shown in the chart), 55% of respondents believe the future lies in green energy, with 41% favoring renewables and 14% choosing Battery Energy Storage Systems (BESS).

In contrast, natural gas (17%) and nuclear energy (16%) are viewed as secondary options, serving largely as transition fuels or baseload supplements. This distribution clearly indicates that under decarbonization pressures, the combination of solar, wind, and storage is becoming the mainstream power solution.

Storage Surge: Resilience Beyond the Grid

Energy storage technology is being hailed as the key to resilience. Nearly three-quarters (74%) of respondents stated that advanced energy storage systems—including batteries, hybrid solutions, and microgrids—are the best way to ensure operations continue during power fluctuations.

Concurrently, energy analyst firm Wood Mackenzie has identified “data centers” as one of the top five trends for global energy storage in 2026. Recently, a battery project even opted to forgo a traditional grid connection, re-tooling to provide off-grid power directly to a data center for revenue generation.

Nuclear Reality Check: High Hopes, Low Adoption

Despite significant buzz in the media, the actual on-the-ground adoption of nuclear power remains low. The report shows that only 14% of developers are actively pursuing modular or small modular nuclear reactors (SMRs) as a viable opportunity.

This suggests that while nuclear is theoretically viewed as the ultimate solution for 24/7 power, regulatory hurdles, construction timelines, and high costs prevent it from being an immediate practical option for most developers, keeping it largely in the planning stages.

Market Forecast: The 2027 Power Cliff

The industry’s outlook is filled with a sense of urgency, with a “strategic correction” appearing inevitable. 63% of respondents anticipate a significant market shift by 2030, driven by the intense competition for limited power resources.

One unnamed banking executive in the report issued a blunt warning: “Once power runs out in 2027 or 2028, that’s where we think deal flow will start to slow down.” This prediction places the power shortage deadline within the next two to three years, leaving a very narrow window for the industry to secure energy assets.

Expert Insight: From “Gold Rush” to Capacity Anxiety

Daniel Farris, partner at Foley & Lardner, described the current situation as a “Gold Rush mentality.” He noted that the frantic scramble to secure power is a major reason why people sense a “bubble,” adding that power at necessary levels will be “really hard to come by” in the next two to three years.

Rachel Conrad, another leader of the firm’s infrastructure team, added that over the next five to ten years, power providers face a binary choice: grow capacity or increase efficiency. Only those who can innovate to solve these efficiency bottlenecks will emerge as winners in this high-stakes game of compute versus kilowatt-hours.