In its latest 2024 report, the International Council on Clean Transportation (ICCT) delivers a revealing snapshot of the state of global electric vehicle (EV) transition. Covering the world’s 21 largest light-duty vehicle manufacturers across six major regions—China, Europe, the United States, Japan, South Korea, and India—this third edition of the ICCT Global Automaker Rating highlights both competitive advancements and concerning slowdowns.

Together, these regions account for 82% of global car sales, and the 21 automakers studied represent 90% of those sales in 2024. The evaluation is based on ten carefully constructed metrics, which examine not only the current market penetration of battery electric vehicles (BEVs) and fuel cell electric vehicles (FCEVs), but also technological readiness, strategic ambition, and efforts toward decarbonization such as battery recycling and green steel usage.

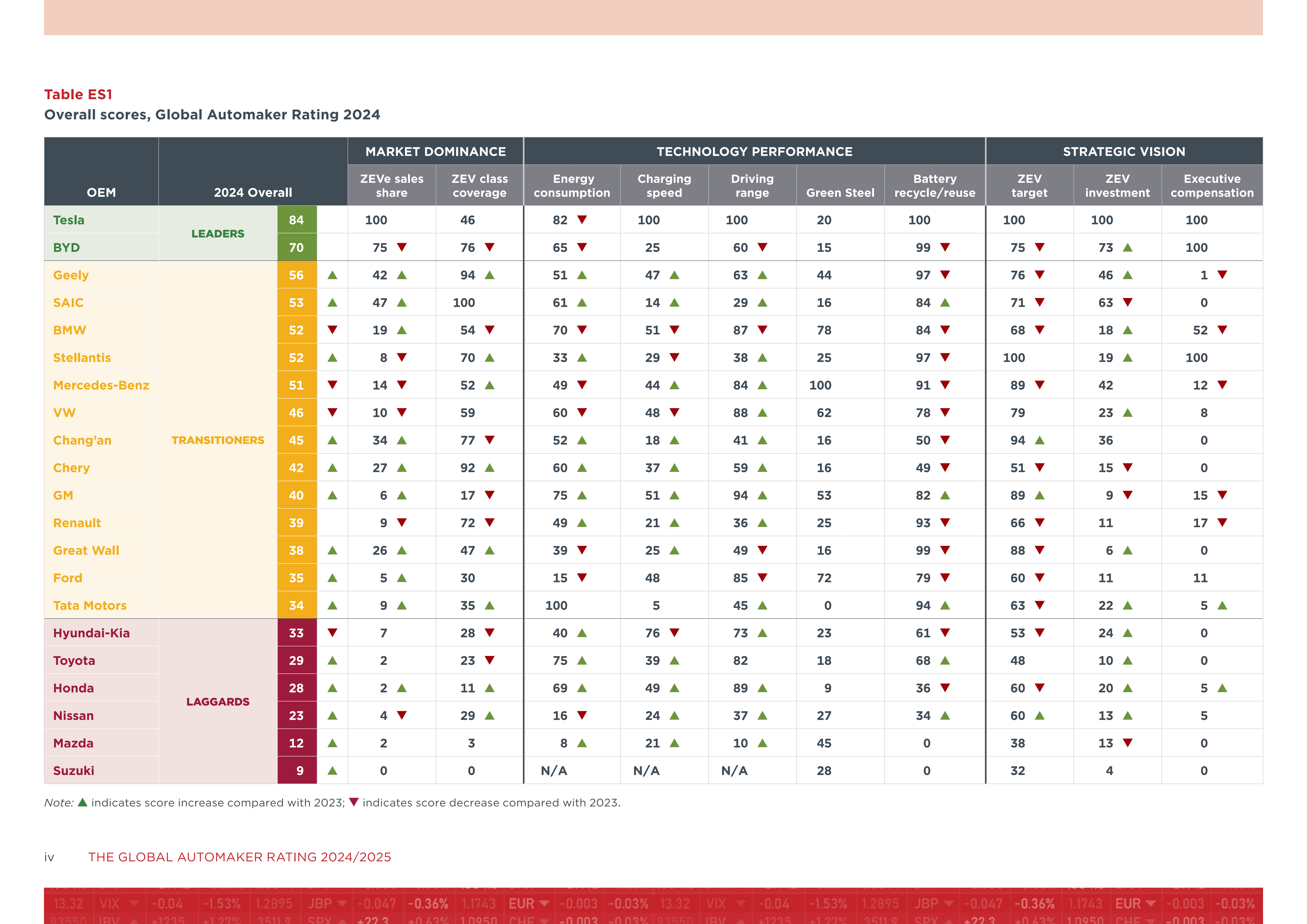

Tesla and BYD Maintain Leadership—But the Gap Narrows

As in the previous year’s report, Tesla and BYD remain in the top two positions, categorized by ICCT as the only automakers that qualify as “Leaders” in the global electric drive transition. Tesla retained its lead, despite flat sales in 2024, while BYD failed to close the gap despite outperforming Tesla in global BEV sales for the first time.

BYD’s 25% increase in BEV sales and 47% growth in combined BEV and plug-in hybrid electric vehicle (PHEV) sales across the six core markets could not offset underperformance in fleet energy consumption and average range, which cost it points in the overall ranking. Tesla, on the other hand, demonstrated consistency across all criteria, allowing it to defend its leadership position despite stagnant volumes.

China’s Rise: Geely, Chery, SAIC Redefine the Midfield

Beneath the top two, the landscape has shifted significantly. Geely (together with its subsidiary Volvo and partner SAIC) and Chery are the standout performers in 2024. These manufacturers, categorized in the “Transitioners” group, have seen notable gains in sales share, product portfolio breadth, and average vehicle performance.

Geely and SAIC have displaced BMW and Mercedes-Benz from the third and fourth positions in the global ranking. Not only did they introduce new high-performance BEV models, but they also ramped up efforts in battery repurposing and recycling—an increasingly important metric given rising scrutiny on end-of-life EV materials.

Chery, meanwhile, achieved one of the biggest leaps. It transitioned from being near the “Stragglers” category in 2023 to securely occupying a central position in the midfield. This reflects increased BEV sales, improved technology, and a growing emphasis on energy efficiency in their new models.

Chinese OEM Changan also performed strongly, consolidating its place in the upper midfield.

European Brands Lose Ground, Despite Heritage and Investment

In contrast to their Chinese counterparts, many European legacy brands are losing momentum. Both BMW and Mercedes-Benz, which were previously in the top four, were displaced due to stagnant product rollouts, limited ZEV (zero-emission vehicle) ambition, and slower improvement in average BEV performance.

Volkswagen (VW) and Stellantis—while still within the upper midfield—did not advance significantly. Despite having robust EV portfolios, their strategic vision and commitment to future investments in zero-emission technologies were found lacking by ICCT standards.

Renault remained static, with no movement in total score, highlighting both consistent performance and a lack of breakthrough. Volvo Cars, under Geely ownership, rolled back its ambitious ZEV goals, contributing to the brand’s weakened overall ranking.

Japan and Korea: Slow Progress, Mixed Signals

Japanese and South Korean manufacturers continued to lag behind their global peers. However, the picture is mixed.

Honda made a breakthrough by introducing its first mass-market BEV, the Prologue, in the U.S. This step helped improve all of its electric performance metrics. Nissan, meanwhile, revised its ZEV targets, detaching BEV objectives from conventional hybrids—a move that clarifies its EV direction and lifted its score.

Hyundai-Kia, on the other hand, fell into the “Stragglers” category, in part because the group failed to disclose tangible progress on battery recycling and reuse—a major penalty under the new 2024 assessment framework. This drop is particularly significant, considering Hyundai’s past reputation as an EV frontrunner.

India’s Tata Motors Climbs, Driven by Portfolio and Recycling

Among the most noteworthy improvements in 2024 is Tata Motors, which became the first automaker in three years to transition from “Straggler” to “Transitioner.” This change was fueled by the introduction of multiple new EV models, as well as the company’s joint efforts with Jaguar Land Rover to expand battery recycling and repurposing initiatives across major markets.

This momentum makes Tata one of the few automakers from outside the U.S., China, or Europe to meaningfully improve its standing in the electrification race.

Electrification Grows, But Strategic Commitment Weakens

Globally, EVs made up nearly 20% of all new passenger vehicle sales in 2024, up from 16% the previous year. From 2022 to 2023, global EV sales grew 26%, and another 27% growth followed from 2023 to 2024. According to the ICCT, this sustained increase demonstrates “remarkable momentum behind electrification.”

However, despite this positive trend in adoption, several automakers retreated from earlier ZEV targets:

- Ford, Tata Motors, Dacia (Renault), Mini (BMW), and Volvo Cars all rolled back or canceled some of their previously announced zero-emission goals.

- Only Changan and Hyundai-Kia marginally increased their electric vehicle targets.

- None of the 21 OEMs significantly increased ZEV investments in 2024, a worrying stagnation as electrification demands capital-intensive scaling.

This mismatch between market growth and strategic investment has raised red flags among climate advocates and regulators alike.

Sustainability Metrics Gaining Weight: Green Steel and Battery Recycling

New to the 2024 ICCT rating are metrics for green steel adoption and an updated framework for battery reuse and recycling. These indicators reflect growing concern not just about vehicle emissions, but about life-cycle carbon impact and resource sustainability.

Many Chinese and European automakers are beginning to address these issues head-on, but disclosure remains limited in many cases. Manufacturers that fail to demonstrate progress in circular economy practices will likely see declining scores in future ICCT evaluations.

Conclusion: A Rapidly Shifting EV Landscape

The 2024 ICCT global EV transition report underscores two parallel realities: electrification is gaining market momentum faster than ever before, yet strategic ambition is cooling across many OEMs. This divergence threatens to undermine long-term climate goals and slow the EV transition just as critical mass is being reached.

While Tesla and BYD remain the indisputable leaders, Chinese carmakers such as Geely, Chery, SAIC, and Changan are now defining the competitive center of the global EV market. In contrast, traditional powerhouses in Europe, Japan, and Korea risk being overtaken unless they accelerate innovation, commit to sustainable practices, and double down on their long-term EV strategies.

The ICCT’s ranking is more than just a scoreboard—it is a call to action for automakers worldwide. The shift to electric is not only a race of units sold, but also of technology readiness, environmental responsibility, and strategic vision.