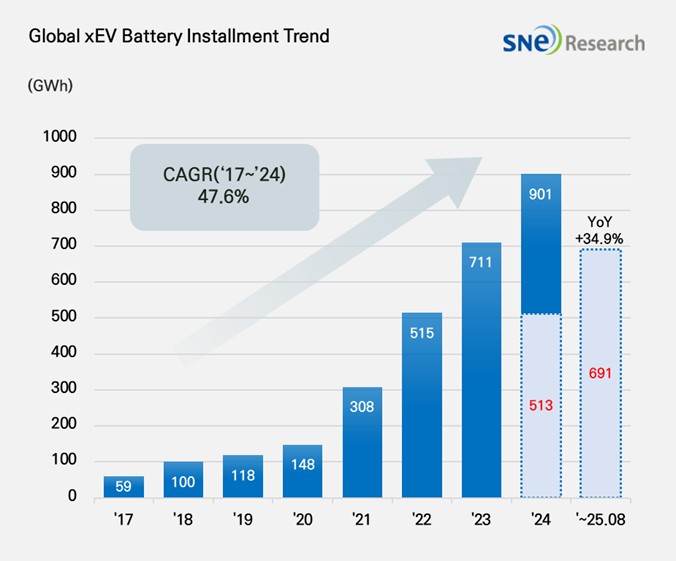

According to SNE Research’s latest “Global Monthly Electric Vehicle and Battery Tracking Report for September 2025,” global electric vehicle (including BEV, PHEV, and HEV) battery installation capacity reached 691.3GWh from January to August 2025, surging 34.9% from 512.6GWh in the same period last year, continuing the robust 47.6% compound annual growth rate (CAGR) momentum since 2017.

Global Battery Market Landscape Transforms: Chinese Companies Establish Dominance

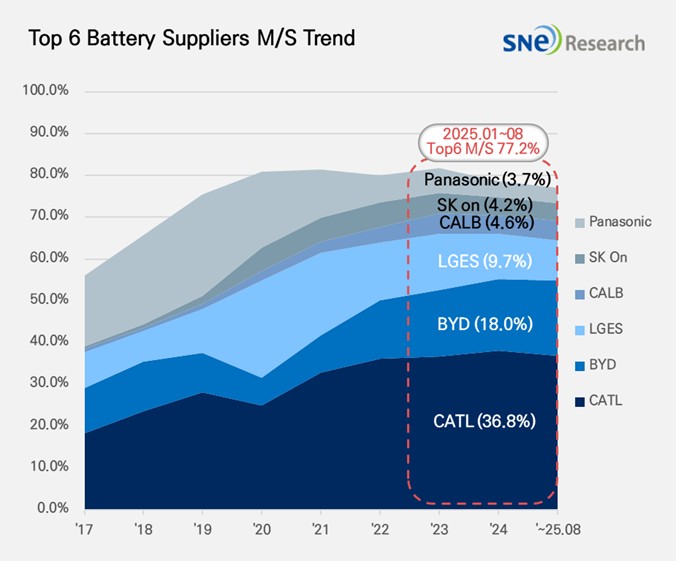

Recent market share data reveals a profound transformation in the global electric vehicle battery market landscape. The top six battery suppliers now command a combined 77.2% market share, indicating further market concentration.

Chinese Companies Rise Powerfully, Capturing Half the Market

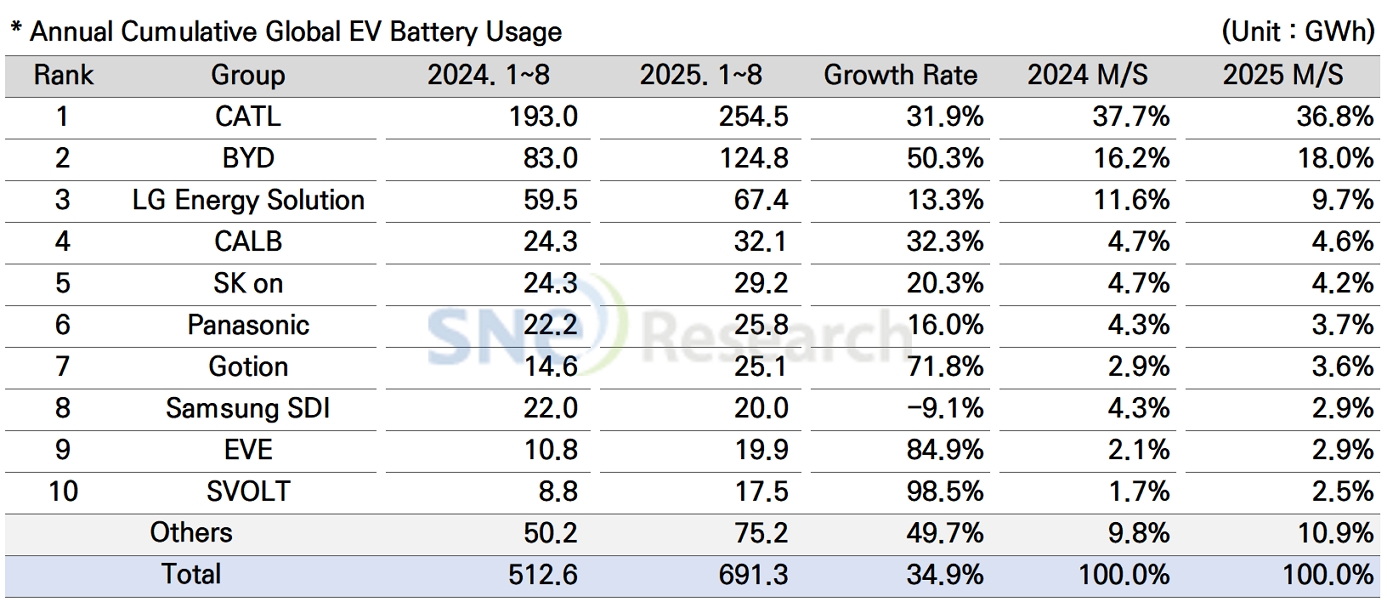

CATL maintains its global leadership with 254.5GWh installation capacity and 36.8% market share, slightly down from 37.7% last year but still achieving a robust 31.9% growth rate. The company not only supplies Chinese brands like Zeekr, AITO, Li Auto, and Xiaomi, but also serves global mainstream automakers including Tesla, BMW, Mercedes-Benz, and Volkswagen.

BYD leverages its unique vertical integration advantage to rank second with 124.8GWh installation capacity, increasing its market share from 16.2% last year to 18.0%, with a remarkable 50.3% year-over-year growth rate. Particularly noteworthy is BYD’s major breakthrough in European markets, where battery installation capacity reached 8.6GWh in the first half of 2025, surging 263.1% year-over-year.

CALB (China Aviation Lithium Battery) ranks fourth with 32.1GWh installation capacity, growing 32.3% year-over-year while maintaining a 4.6% market share.

Emerging Forces Rise Rapidly

Second-tier Chinese battery manufacturers demonstrate exceptional performance:

- Gotion High-Tech: 25.1GWh installation capacity, up 71.8% YoY, market share increased from 2.9% to 3.6%, ranking seventh

- EVE Energy: 19.9GWh installation capacity, up 84.9% YoY, achieving 2.9% market share, ranking ninth

- SVOLT Energy: 17.5GWh installation capacity, surging 98.5% YoY, with 2.5% market share, ranking tenth

The rapid growth of these three companies demonstrates the deep strength and enormous potential of China’s battery industry.

Korean Big Three’s Share Continues Declining

In stark contrast to Chinese companies’ strong performance, the combined market share of South Korea’s Big Three battery manufacturers (LG Energy Solution, SK On, Samsung SDI) dropped from 20.6% last year to 16.8%, a decrease of 3.8 percentage points.

LG Energy Solution (LGES) maintains third place globally with 67.4GWh installation capacity, up 13.3% year-over-year, though market share declined from 11.6% to 9.7%. The company primarily supplies Tesla, Chevrolet, Kia, and Volkswagen. Due to slower sales of Tesla-related models, LGES’s supply to Tesla decreased 15.8% year-over-year. However, strong global sales of the Kia EV3 and expansion of Chevrolet Equinox, Blazer, and Silverado EV Ultium platform vehicles in North America provide growth support.

SK On ranks fifth with 29.2GWh installation capacity, up 20.3% year-over-year, though market share fell from 4.7% to 4.2%. Major clients include Hyundai Motor Group, Mercedes-Benz, Ford, and Volkswagen. The Hyundai IONIQ 5 and Kia EV6 are its primary supported models, while stable sales of Volkswagen ID.4 and ID.7 also contribute volume. Although Ford F-150 Lightning sales slowed, growth in Explorer EV drove SK On’s supply to Ford up 13.0% year-over-year.

Samsung SDI shows the weakest performance with 20.0GWh installation capacity, down 9.1% year-over-year, as market share dropped from 4.3% to 2.9%, falling to eighth place. The company primarily supplies BMW, Audi, and Rivian. While BMW i-series models and Audi Q6 e-Tron brought some volume, Rivian’s newly launched standard range versions adopt Gotion’s LFP batteries, impacting Samsung SDI’s supply share.

Panasonic Focuses on North America Strategy

Panasonic ranks sixth with 25.8GWh installation capacity, up 16.0% year-over-year, holding a 3.7% market share. As Tesla’s major supplier, Panasonic is accelerating supply chain reorganization to focus on the North American market. Facing U.S. tariff barriers on Chinese batteries and raw materials, Panasonic is working to reduce dependence on Chinese materials and expand local procurement to ensure competitiveness in the North American market.

Market Outlook: From Growth to Consolidation

Historical trend charts show the global electric vehicle battery market has grown explosively from 59GWh in 2017 to 691GWh in the first eight months of 2025. The 2017-2024 CAGR reached 47.6%, with full-year 2025 installation capacity expected to exceed 801GWh.

However, the market landscape is undergoing profound changes:

- Rising Market Concentration: Top six manufacturers’ market share has shifted from fragmented to concentrated, with clear dominance effects

- Chinese Companies’ Dominance Established: Chinese companies’ combined market share now exceeds 60%

- Technology Route Differentiation: LFP batteries rapidly expand with cost advantages, challenging traditional ternary batteries

- Accelerated Regional Production: Countries strengthen local supply chain construction, making cross-border factory construction a trend

Industry Chain Challenges and Opportunities Coexist

Behind the rapid growth of the global secondary battery market lie numerous challenges:

Supply Chain Security Becomes Focus: As the G7 and EU consider price caps and export controls on rare earth elements, stable supply of critical minerals has become a core constraint on industry development. The U.S. is strengthening government-led lithium supply chain construction through measures like acquiring stakes in Lithium Americas.

Intensified Local Production Competition: Chinese battery companies are rapidly expanding global influence through overseas factory construction, such as CATL building facilities in Spain, Hungary, and Germany, bringing both technological and cost pressures to local companies.

Enhanced Sustainable Development Requirements: Battery manufacturers must not only expand capacity but also ensure compliance, diversify material sources, and advance sustainable design and recycling system construction.

In this context, only companies with technological innovation capabilities, flexible supply chain management, and sustainable development strategies can stand out in medium to long-term competition. As global new energy vehicle penetration rates continue rising, battery industry competition will intensify further, and market landscape restructuring will continue.