The British Auto Industry on the Brink

In January 2026, the newly released UK Gigafactory Commission Report issued a severe warning to the government: battery manufacturing is no longer just a technological or energy issue, but a strategic imperative essential to the nation’s economic survival.

The report highlights that while the UK has ambitious goals for the transition to electric vehicles (EVs), it has fallen dangerously behind global competitors in building a critical battery supply chain.

Without a rapid turnaround in the next five years, the UK’s proud automotive manufacturing sector faces the very real risk of “de-industrialization.” Production could shift overseas, leaving the domestic workforce behind.

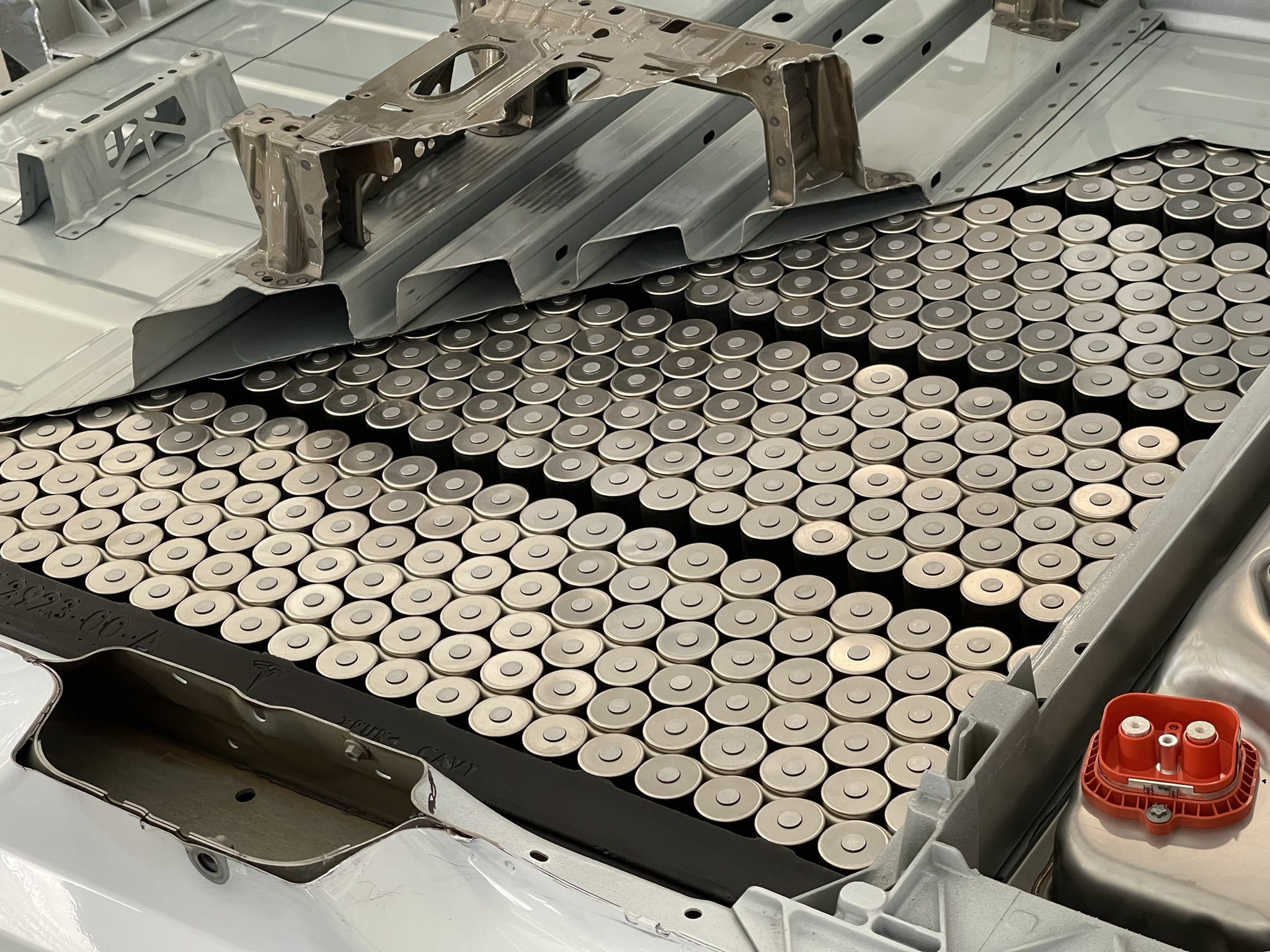

Currently, the UK has secured only two major gigafactory projects: the AESC Envision Plant 2 in Sunderland and the Tata Group’s Agratas facility in Somerset. Compared to the colossal future demand of the UK automotive sector, this is a drop in the ocean.

The Supply-Demand Chasm: 130 GWh Needed vs. 31 GWh Reality

According to data from the Faraday Institution and the Commission, the UK will require approximately 130 GWh of battery capacity by 2035 to sustain domestic EV production levels.

However, the current reality is harsh. Even accounting for the confirmed AESC and Agratas projects, the UK’s domestic battery capacity is projected to reach only around 31 GWh by 2030.

This massive supply gap implies that British car manufacturers will be forced to rely heavily on imported batteries. This reliance is not just a logistical cost; it poses a fatal regulatory risk.

Importing batteries will violate the Rules of Origin (RoO) within the UK-EU trade agreement. Without domestic battery production, UK-made EVs will face steep tariffs when exported to the EU, destroying their price competitiveness.

Progress Report: AESC Goes Live, Agratas Under Construction

Despite the grim overall picture, there are bright spots. The report confirms that the AESC Plant 2 in Sunderland officially began operations in December 2025.

This facility is currently the UK’s largest operating battery plant, providing critical support for Nissan’s electrification transition and serving as a proof of concept for British manufacturing.

Meanwhile, Tata Group’s £4 billion Agratas gigafactory is under aggressive construction in Bridgwater, Somerset. Following the completion of steelwork in 2025, the site is on track to begin battery production in late 2027.

However, the report emphasizes that these two projects alone cannot prop up the entire industry. The UK needs more “anchor” projects, specifically requiring global OEMs to commit to UK EV production to drive further battery demand.

A Strategic Pivot: From “Open for Business” to “Active Intervention”

The Commission proposes a core strategic shift: the UK government must abandon its passive “Open for Business” stance in favor of a proactive “interventionist mindset.”

The government cannot simply wait for investors; it must act like an investment bank, actively brokering deals. The report suggests a “Tripartite Approach,” bundling the OEM (demand), battery maker (tech), and material supplier (supply chain) into a single investment package.

To execute this, the report recommends appointing a specific Cabinet Minister who reports directly to the Prime Minister. This role would lead cross-departmental investment efforts, cutting through bureaucracy to accelerate decision-making.

Critical Reforms: Energy Costs and the ZEV Mandate

The report’s most controversial yet pragmatic recommendations involve two key policy areas. First is the crippling cost of energy. UK industrial electricity prices are roughly double the EU average, a fatal disadvantage for energy-intensive battery manufacturing.

The Commission advises that the government must significantly increase subsidies and relief for Energy Intensive Industries (EIIs) to bring UK costs in line with European competitors. Without competitive energy, tax breaks are insufficient.

Second, the report calls for a recalibration of the “Zero Emission Vehicle (ZEV) Mandate.” Current policy requires 80% of new cars sold in the UK to be zero-emission by 2030. The Commission views this as overly aggressive and potentially damaging.

They argue this target could force manufacturers to withdraw from the UK market to avoid fines. The report suggests lowering the 2030 mandatory ratio to 50-60%, aligning it with market reality and EU trajectories while buying time for the supply chain to mature.

Embracing Pragmatism: A New Stance on China

Against a backdrop of complex geopolitics, the report adopts a pragmatic stance regarding China’s dominance in the battery supply chain. It suggests a strategy of “Conditional Collaboration.”

This means that, provided national security and supply chain transparency are guaranteed, the UK should welcome Chinese battery technology and capital.

The report even suggests using the UK as a “bridgehead” for Asian manufacturers looking to enter the European market, trading market access for technology transfer and local job creation.

This reflects an industry consensus: completely severing ties with the Chinese supply chain is unrealistic and would severely decelerate the UK’s own electrification progress.

Infrastructure and Talent: Paving the Way for Growth

Beyond factories, the report highlights the need for ready infrastructure. Addressing slow planning permissions, it proposes a “Strategic Sites Accelerator” to provide “shovel-ready” land with pre-approved power and water connections.

On the human capital front, battery manufacturing requires a massive influx of skilled labor. The report recommends launching a national talent program similar to “Destination Nuclear.”

This would utilize apprenticeships and retraining schemes to build a specialized battery workforce, ensuring that once factories are built, the UK has the engineers and technicians to run them efficiently.

Conclusion: The Final Window of Opportunity

The UK Gigafactory Commission Report is not just an industry analysis; it is an urgent blueprint for action. It states clearly that the UK has no room left for error in the global battery race.

With 2030 fast approaching, the window for the government and industry to act is rapidly closing. If the recommendations to attract new gigafactories are not implemented within the next 12 to 24 months, the opportunity may be lost forever.

The choice is stark: intervene decisively to win the future, or hesitate and watch the industry drift away. For the UK, this is a battle it cannot afford to lose.