Prologue: From Dots on a Map to Future Trendlines

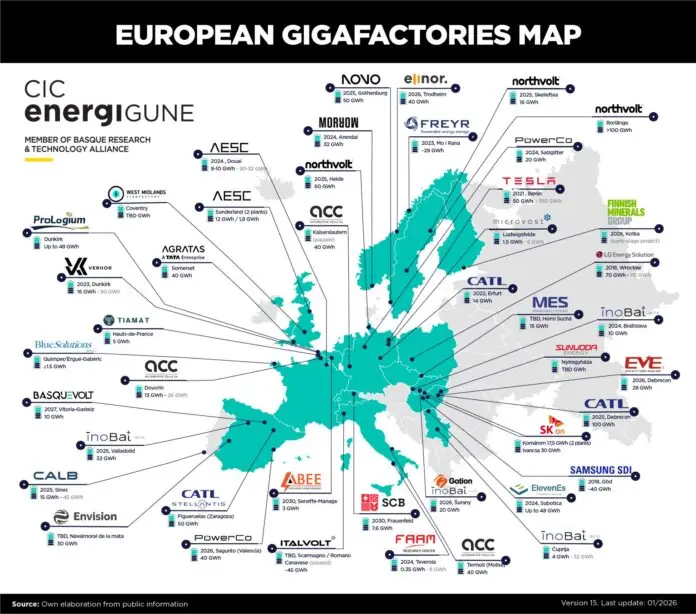

The “European Gigafactories Map” (V15, 2026) released by CIC energiGUNE depicts the current “Warring States” period of European battery manufacturing. However, this is merely the prologue.

When combined with the latest industry forecast data, what we see is not just a shift in geographical coordinates, but a capacity marathon sprinting toward 2040. The region is undergoing an industrial revolution, attempting a colossal leap from GWh (Gigawatt-hours) to TWh (Terawatt-hours) to support its automotive ambitions.

The Core Battlefields: Germany and Hungary (Status Quo)

According to the 2026 map, Germany firmly sits as the “heart” of European battery manufacturing. As a fortress of traditional automotive industry, it hosts giants like Tesla, PowerCo, Northvolt, and CATL.

This layout, often characterized by “close-quarters combat” near OEMs (Original Equipment Manufacturers), aims to minimize logistics costs and enable Just-In-Time delivery.

Simultaneously, Hungary is rapidly rising as the “Second Pole.” The dense clustering of markers in the east reveals it as the bridgehead for Asian battery titans—such as CATL, Samsung SDI, and EVE—to enter Europe. Leveraging favorable policies and costs, Hungary has become the critical hub connecting Eastern technology with Western markets.

Data Perspective: The 2040 “TWh” Ambition

If the map shows us “where” to build, the latest forecast data answers “why” the scale must be so massive.

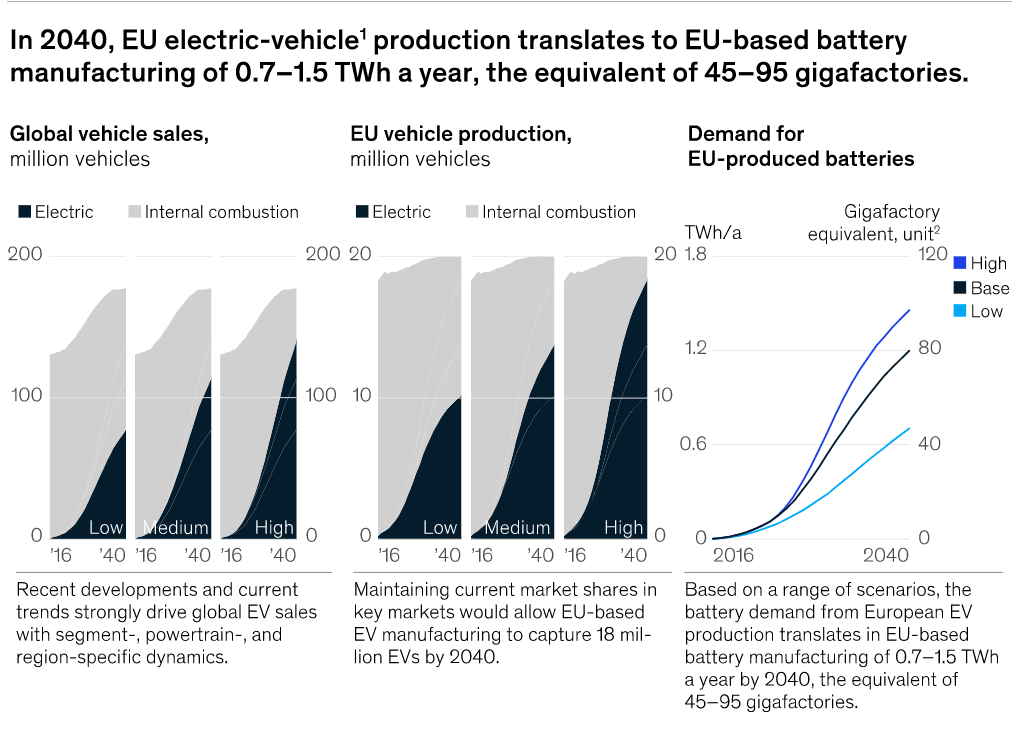

Predictive models indicate that to maintain current market shares amidst a global surge in electric mobility, EU-based electric vehicle manufacturing must reach 18 million vehicles annually by 2040.

This massive vehicle production translates into an astronomical demand for batteries:

- Base Scenario: Demand for EU-produced batteries will hit approximately 1.2 TWh/year.

- High Scenario: This figure could soar to 1.5 TWh/year.

To satisfy this appetite, Europe needs more than just the currently planned projects. It ultimately requires an industrial base equivalent to 45 to 95 standard gigafactories. The current construction boom is essentially an attempt to fill this looming supply-demand chasm.

Key Contenders: Local Challengers vs. Asian Giants

Against this backdrop, every strategic move matters.

European Local Forces: Companies like Northvolt and ACC carry the hopes of European “strategic autonomy.” They face the dual challenge of scaling production capacity while racing to secure technological leadership in a market that will eventually demand nearly a hundred factories.

Asian Expansion: Facing a potential 1.5 TWh market in 2040, the European expansion of Asian firms like CATL and Envision AESC is urgent. Their deployments in Germany, Hungary, and the UK are essentially moves to lock in the supply chains for those 18 million future European EVs early in the game.

Supply Chain Security: The Geopolitical Necessity

Behind the map lies a deep European anxiety regarding “energy security,” and the data charts quantify this anxiety.

With forecasts showing EU electric vehicle production exploding across “Low, Medium, and High” scenarios by 2040, localized battery supply is no longer optional—it is mandatory.

Relying on external supply chains cannot sustainably support the manufacturing of tens of millions of vehicles annually. Policies like the EU’s Net Zero Industry Act are designed to ensure these 45-95 factories actually materialize on European soil.

The Reality Gap: Planning vs. Execution

While the data draws a perfect exponential growth curve—rising steeply from 2016 to 2040—reality is fraught with friction.

Construction delays, high energy costs, skilled labor shortages, and raw material volatility act as barriers preventing blueprints from becoming reality. Whether the projects on the 2026 map can successfully translate into the 1.5 TWh needed for 2040 remains the biggest suspense for the European industry over the next fifteen years.

Conclusion: Reshaping the Global Energy Order

The CIC energiGUNE map and the 2040 forecast report together form Europe’s “battle map” for the energy transition.

They tell us that the European battery industry is not just building factories; it is constructing a new ecosystem worth hundreds of billions of Euros. From today’s tens of GWh to the future’s 1.5 TWh, this transformation will fundamentally reshape the global map of energy power.