As policy shifts driven by the One Big Beautiful Bill Act (OBBBA) and rising project costs mount pressure on solar and wind projects, investors in the ERCOT (Electric Reliability Council of Texas) market are increasingly pivoting toward battery energy storage systems. New data from Swiss analytics firm Pexapark shows that forward values for battery storage are hitting record highs, while solar and wind power purchase agreements (PPAs) face an increasingly widening bid-offer spread.

Battery Storage Arbitrage Returns Surge

Pexapark reports that with BESS in ERCOT now relying on energy arbitrage for the majority of their revenue, the arbitrage opportunity over the next ten years advanced by double digits in three out of four ERCOT hubs compared to the same quarter last year. Following a lengthy period of underperformance, this finding points to an increasingly bullish view of BESS over the long-term as load growth and renewables penetration continue to widen intraday spreads.

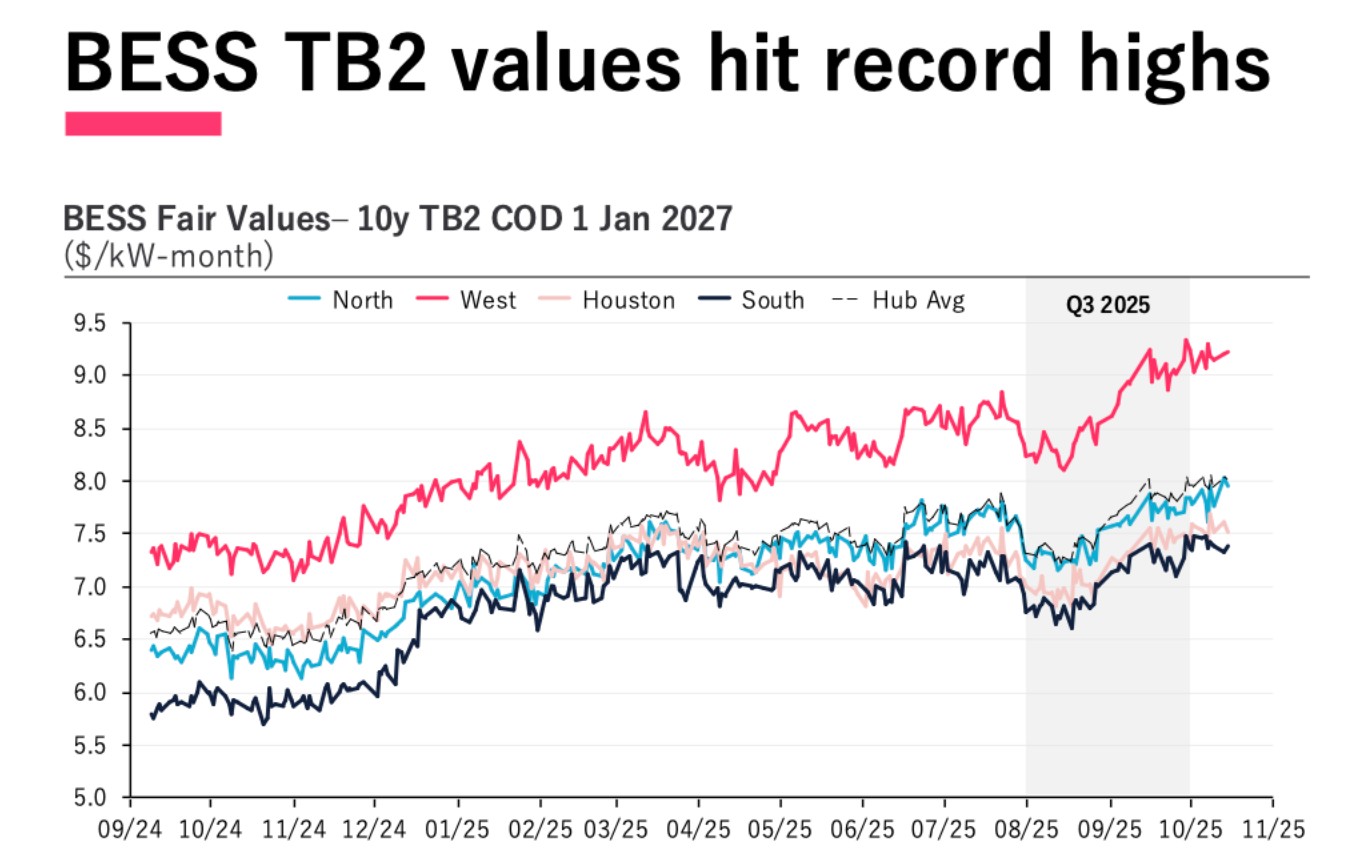

According to the chart provided by Pexapark, the fair values for 10-year TB2 with commercial operation date (COD) of January 1, 2027, reached approximately $9.2/kW-month in Q3 2025 for the West hub—a record high that significantly exceeds other hubs. The North hub recorded around $8.0/kW-month, while the South hub and Hub Average reached approximately $7.4/kW-month and $7.9/kW-month respectively.

At the same time, BESS toll offers stayed mostly flat or declined. This convergence—rising value levels combined with competitive, stable offer pricing—points to a potentially growing opportunity in BESS dealmaking, Pexapark notes.

“Expected load growth coupled with high levels of solar penetration mean that intraday spreads in ERCOT will, in general, get wider, with consistent midday dips and increasingly prominent shoulder hour spikes. This dynamic strengthens the long-term economic rationale for BESS even if recent summers saw decreased levels of price volatility,” said Yaniv Yaffe, Pexapark product manager.

Record-Breaking BESS Deployment in ERCOT

Despite market volatility and a 60% year-over-year revenue decline in the first half of 2025, Modo Energy finds projects can still be profitable and meet investor return thresholds, particularly with favorable locations, duration (2 hours+), and offtake agreements.

Therefore, BESS buildout in ERCOT shows no signs of slowing down. According to Modo’s recent reports, a record 2 GW of battery energy storage capacity began commercial operations in ERCOT in Q3 2025, marking the market’s largest deployment of battery capacity in a single quarter. ERCOT’s operational battery capacity has now reached 12,052 MW in rated power and 19,442 MWh in energy capacity.

The 21 new battery storage projects that came online in Q3 2025 were distributed across ERCOT’s load zones. Six of these exceeded 100 MW, with the largest being esVolta’s Anole BESS (247 MW | 480 MWh) in the North zone, Gridstor’s Evelyn BESS (220 MW | 440 MWh) in Houston, and Engie’s Cachi BESS (200 MW | 400 MWh) in the South.

Engie deployed the most capacity in Q3, with five two-hour duration batteries over 50 MW achieving commercial operations, bringing 788 MW to market. This represents a notable change for Engie, which has historically held a 30-strong portfolio of exclusively 1-hour-duration batteries. Engie’s total ERCOT portfolio is now up to 2,524 MW, continuing its position as the largest battery owner in Texas, with over twice the capacity of the next owner (Enel Green Power at 1,147 MW).

Solar and Wind PPA Market Struggles

In stark contrast to the thriving battery storage sector, solar and wind PPAs have experienced a more difficult market environment since the passage of the OBBBA. While a 7% rise in the forward market drove the fair value of wind and solar PPAs higher in Q3, offer prices for such contracts rose even more: 12% for wind PPAs and 13% for solar PPAs, Pexapark finds.

The result is an increasingly illiquid PPA market. Pexapark tracks only three ERCOT PPAs which were publicly announced in Q3, representing fewer than half the number of deals signed in the same quarter last year.

The higher offer prices for wind and solar PPAs reflect an increasingly hostile regulatory environment. The OBBBA is phasing out billions in clean energy tax credits by mid-2026 while imposing strict sourcing restrictions on Chinese components. Although safe harbor provisions were preserved, the narrow compliance windows are straining developers and pushing up project costs.

The OBBBA terminates eligibility for 45Y and 48E clean electricity production and investment tax credits for wind and solar projects placed in service after December 31, 2027, with an exception for projects that begin construction within twelve months of the legislation’s enactment. The act also mandates more stringent domestic content percentages: 40% (20% for offshore wind) if construction began before June 16, 2025; 45% (27.5% for offshore wind) if construction begins between June 16, 2025, and January 1, 2026; 50% (35% for offshore wind) if construction begins during 2026; and 55% if construction begins after December 31, 2026.

“The ERCOT market is facing temporary but acute policy-driven shocks that have created a pricing gap between project costs and buyers’ willingness to pay. For wind and solar, the price gap is now significant and is contributing to the shift in focus toward BESS,” said Luca Pedretti, COO & co-founder of Pexapark.

Far-Reaching Policy Impacts

According to analysis by Energy Innovation Policy & Technology LLC, the House OBBBA as passed is projected to increase annual energy bills by $3.7 billion across Texas households annually in 2030, swelling to more than $9.8 billion in higher energy costs by 2035, for a total of $38.06 billion during the budget window of 2025 to 2034. This is due to higher dependence on fossil fuels and higher fossil fuel prices.

The legislation would also cost Texas’s workforce 61,100 jobs in 2030 and nearly 121,600 jobs in 2035 as new investment in domestic energy and manufacturing falters. Between 2025 and 2034—the Reconciliation budget window—cumulative GDP would shrink by $87 billion in Texas.

Market Outlook and Investment Opportunities

Despite the challenges, the ERCOT market is undergoing structural transformation. In October 2025, during the peak BESS daily discharge hour, batteries dispatched an average of 4.8 GW of power, up from just 0.37 GW in October 2023. This growing significance of battery storage is closely tied to broader trends in renewable generation across the ISO.

Notably, Houston is expected to add 9.6 GW of BESS capacity by the end of 2027, marking a fivefold increase. This growth is occurring despite the hub accounting for less than 6% of ERCOT’s forecasted renewable capacity. In contrast, the West Hub is projected to see the largest renewable buildout of the ERCOT hubs over the same period, with over 45 GW of planned operational capacity, yet it is slated to see the least BESS deployment. This disconnect signals a shift from the traditional trends of co-locating battery storage near intermittent renewable generation.

One possible driver is that peak pricing events in ERCOT’s load centers are allowing for profitable pricing arbitrage opportunities. The economic incentive for this shift in location strategy becomes apparent when comparing regional trends at the Hub level.

For investors, this market shift presents both opportunities and challenges. ERCOT’s “first-ready, first-served” interconnection model, with a typical timeline of 18 to 30 months for large projects, enables faster deployment than CAISO’s cluster study model. While not every queued project reaches completion, developers are able to move forward without waiting on centralized procurement or long-term contracts—accelerating progress for the most viable and strategically located assets.

For battery storage projects, the duration profile is evolving. By late 2024, six of the top seven BESS operators in ERCOT were averaging more than 1.5 hours per project. This reflects a shift toward two-to-four-hour systems, aimed at both arbitrage and emerging products.

Conclusion

The ERCOT market is at a critical juncture in the energy transition. While policy changes brought by the OBBBA have created near-term pressures on solar and wind projects, battery storage is benefiting from growing market demand and favorable economic conditions. As Texas continues its rapid population and economic growth, electricity demand is expected to increase significantly, providing a long-term value proposition for storage systems.

For market participants, the key is adapting to the changing policy environment while seizing new opportunities presented by battery storage. Projects that can deploy long-duration storage systems in favorable locations, secure competitive offtake agreements, and effectively manage market risks will succeed in this dynamic market.